In 2008, both Ireland and the United States of America bailed out their banks. The big difference is that the American politicians did not trust their bankers with a vast amount of public money. So they set up a special police force to make sure the taxpayers didn’t get ripped off.

Following the money trail gave them a license to snoop inside all of the banks. So far, America's bailout cops have put more than 200 people behind bars, and recovered $10 billion for the taxpayer – half of it from Goldman Sachs.

This is accountability, American style.

On 29 September 2008, the banking crisis exploded. That evening, RTÉ’s 6.01 news stayed on air with live pictures from the US Congress, as an emergency bank bailout bill failed to get enough votes to pass. That sparked the biggest one day drop ever recorded by the Dow Jones Index.

Within an hour, a meeting began in Government buildings in Dublin that would end with a blanket government guarantee of the Irish banks being issued just before the European Stock Markets opened the following morning.

The US bailout bill – establishing the Troubled Assets Relief Programme (TARP) - passed on 3 October, authorising the US government to spend up to €700bn to stabilise the financial system by taking stakes in banks and buying up mortgage backed securities that were tanking, as subprime borrowers defaulted on home loans they should never have got.

In the few, frantic days that it took to swing the votes in congress, numerous changes to the TARP bill were made.

One of them, insisted on by Congress, was the establishment of a special police force to keep an eye on the taxpayers money that was going to be used to bail out the banks. And so SIGTARP was created – the Special Inspector General of the Troubled Assets Relief Programme.

Not everybody welcomed SIGTARPs creation: its first boss left after three years over a running dispute with then President Obama's Treasury Secretary Timothy Geithner. In the sniping campaign he claims was directed against the new Agency, it took flack in some newspapers for doing what all American police forces do: it bought guns and bullet proof vests for staff going on raids. Bankers expressed outrage that they were going to be treated like...well, criminals!

SIGTARP took the view that when they wanted to get inside a bank to see what was going on, nobody was going to stop them.

Back in Ireland, the Bank Guarantee - originally touted as the cheapest bank bailout in the world - came home to roost with a vengeance in 2010, when the banks needed to be recapitalised to the tune of €64bn - about 25% of GDP.

Then the state needed to be bailed out to the tune of €67bn by the EU and IMF. NAMA was set up to take troubled assets off the bank’s balance sheets. The taxpayer was on the hook for a potential €31 billion extra, with a brand new state agency having to deal with the biggest sharks in the sharkpool of Irish Commercial Real Estate.

In all of the conditions imposed by the Troika, in all of the resolutions and laws voted in the Dail, none of them insisted on setting up a special unit to mind the taxpayers money. In an unprecedented crisis, an unprecedented amount of taxpayers money was funnelled into private interests. But in Ireland, minding that money was entrusted to institutions that had precedent - the same old-same old.

In the US, SIGTARP had a license to investigate the goings on in any bank that was bailed out with public money - and that was pretty much all of them. And it could investigate any other scheme, arrangement or contract that used public money to deal with the consequences of the collapse of the credit fuelled property market.

It built slowly, developing its modus operandi (based on computer analysis of bank records, looking out for "red flags" - events that have led to the unearthing of frauds elsewhere). But its latest quarterly report makes for interesting reading.

In it, the agency's director, Christine Goldsmith Romero, said "SIGTARP created a new law enforcement playbook to catch up to financial institutions fraud. SIGTARP's intelligence-driven playbook identifies insider crime without relying on the regulator or the bank to sound the alarm. We actively search for crime using industry, financial and human intelligence. Every case is different, but we capitalise on similarities to root out crime. We understand complex bank records, and bank operations, and use intelligence to identify anomalies and trends. Technologies analyse mountains of electronic data, and find digital footprints that serve as powerful evidence of criminal intent".

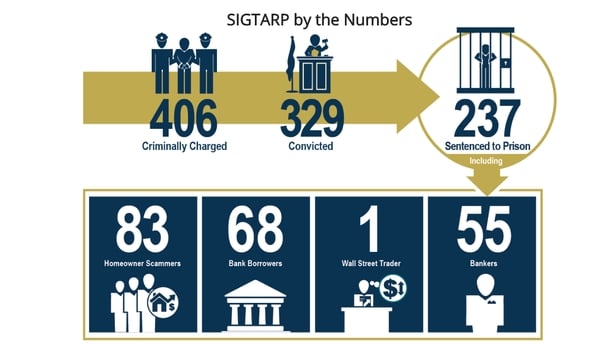

So far, the Agency has brought criminal charges against 406 individuals. 329 of them have been convicted, and 237 of them have been sent to prison.

Among those sent to prison, the biggest number - 83 - have been "Homeowner Scammers" - conmen who stole money from people who had run into mortgage distress by promising them better terms, or access to Federal assistance (for an upfront fee).

The next biggest category to go to jail - 68 - were bank borrowers. People who had borrowed money, usually mortgages, from banks which they then tried to defraud – a reminder that not everyone who got a mortgage and faced repossession was a wholly blameless victim: some of them too tried to profit from the situation and extract personal gain from other people’s loss.

Actual bankers were only the third biggest number of people jailed for bank related crimes. 55 of them were sent to the big house for various terms, ranging from a few months to 15 years. To Irish eyes, grown perhaps too accustomed to billions, the amounts they were sent down for look quite modest (see below).

One wall street trader was also jailed on foot of a SIGTARP investigation (out of six charged).

"Finding TARP related crime and investigating to uncover evidence that the Justice Department needs to prosecute takes time", says Christine Goldsmith Romero.

"That's why the statute of limitations for bank fraud is 10 years. In fiscal years 2016 and 2017, the Department of Justice indicted or filed a criminal complaint against 99 defendants who were investigated by SIGTARP.

"SIGTARP investigations have also resulted in significant DOJ enforcement actions finding violations of the law by nine corporations that received TARP dollars, such as Goldman Sachs, Bank of America, JP Morgan Chase, Morgan Stanley, Ally Financial, Sun Trust Bank, Fifth Third Bank, Jefferies & Co, and General Motors."

"Our top law enforcement priorities are to bring justice to bankers who commit fraud at banks where taxpayers lost money," she says. Below we reproduce extracts from some of SIGTARPS news releases from the past 18 months, to give a flavour of the kind of crimes these money cops have investigated and brought to trial.

25 September 2017

"With the sentencing of mortgage banker Ben Leske, 15 bank employees have now faced justice for a conspiracy that directly contributed to Pierce Commercial Bank’s failure and the loss of $6.8 million in TARP bailout funds," said Special Inspector General Goldsmith Romero.

"Ringleader Shawn Portmann, who was sentenced to ten years in federal prison for his crimes, created a culture at PC Bank Home Loans, Pierce Commercial Bank's mortgage lending office, where all loan applications were expected to be approved, regardless of the applier's ability to repay. Under this 'close every loan' culture, he and his co-conspirators submitted false and fraudulent documents showing borrowers who appeared qualified for mortgages when in fact they were not. As a result, PC Bank Home Loans greatly expanded the residential mortgage lending operations of Pierce Commercial Bank prior to the financial crisis from no more than $3.9m a month to nearly $500m a year.

"Those whose crimes deepened the damage from the 2008 financial crisis deserve to be punished just like any other criminal," said U.S. Attorney Annette L. Hayes.

"This defendant and 14 other well-paid bank employees from loan officers to bank vice presidents forged documents and made false statements to close loans they knew were not sound. The result was the collapse of Pierce Commercial Bank and the expenditure of nearly $7m of taxpayer funds to address the financial mess these defendants left behind."

A sort of comptroller and auditor general with guns

As well as going after errant bankers, SIGTARP has broadened its remit to looking into other government funded schemes that were set up to deal with the fallout from the financial crisis.

One of them is the "Hardest Hit Fund" which helps to keep workers who have lost their jobs in their homes by subsidising mortgage repayments for a period. It has figures in cities where General Motors laid off workers as part of its Federally Funded restructuring programme.

Another scheme paid for the demolition and removal of blighted properties (perhaps this is where we got the notion that ghost estates were going to be demolished back in 2010). In these cases SIGTARP has acted like a sort of Comptroller and Auditor General with guns, doing deep dive audits to monitor value for money and guard against the rip-off of taxpayers money. It recently won an award for exposing a contractor feathering his own nest in Nevada, one of the states that suffered one of the biggest housing busts in America (and used a model in the Irish bank bailout as the nearest thing in scale to what happened here.)

19 October 2017

The Office of SIGTARP today announced that its audit team was recognised for finding that the contractor managing Nevada's Hardest Hit Fund wasted and abused $8.2m in TARP funds. The audit award for excellence was given by the Council of the Inspectors General on Integrity and Efficiency, an independent organisation that addresses integrity, economic, and effectiveness issues within the federal government.

They found that the Nevada Affordable Housing Assistance Corporation (NAHAC), the contractor selected by the Nevada Housing Division to manage Hardest Hit Fund, used the program as a cash cow for every expense imaginable while all but stopping admitting new homeowners.

That is the textbook definition of waste and abuse. SIGTARP’s findings included: A $500 per month car allowance for the CEO who drove a Mercedes Benz; A $20,000 severance package for a terminated CEO; More than $15,000 for employee bonuses, gifts, holiday parties, a manager outing at a high-end cocktail bar, gift cards, and regular staff breakfasts and lunches; More than $160,000 in block-billed legal fees, and costs for a private investigator; Nearly $40,000 for auditors to clean up the contractor’s books; and more than $100,000 in moving fees, excessive rent, and lawyers' fees to move to nicer office space only to break the lease and move out less than a year later.

In 2015, when much of the wasteful and abuse spending occurred, NAHAC kept almost one HHF dollar for every one it distributed to homeowners. It only approved 117 homeowners out of 688 applications.

Common or garden banksters

But most of the perps put away by SIGTARP are small-fry Banksters of the common or garden variety:

24 April 2017

Lamar Cox, 73, of Nashville, Tenn., former Chief Operating Officer and Board of Directors member of now defunct Tennessee Commerce Bank (TCB), pleaded guilty on 21 April 2017, to causing the bank to make a false statement to the Federal Deposit Insurance Corporation (FDIC), announced Christine Goldsmith Romero, Special Inspector General for the Troubled Asset Relief Program (TARP) and Jack Smith, Acting US Attorney for the Middle District of Tennessee.

TCB was closed by federal regulators on 27 January 2012, due to its failing financial condition. "In 2009, at the height of the financial crisis and while Tennessee Commerce Bank was in TARP, Lamar Cox had an important decision to make: as required by law, he could tell the truth to bank examiners about loan losses or hatch a scheme to make the bank appear healthier than it actually was," said Special Inspector General Goldsmith.

Romero said: "Cox chose lies and deception to understate the bank's losses and inflate its income. And, as the chief operating officer and member of the bank's board of directors, he made that decision to deceive in a key position of authority with decades of experience in finance, compliance, and lending. TCB received a $30m bailout from TARP, all of which was lost when the bank failed. I commend Acting US Attorney Jack Smith and Assistant U.S. Attorney Thomas J. Jaworski for standing united with SIGTARP against crime by this TARP banker."

7 march 2017

David Gotterup was sentenced at the federal courthouse in Brooklyn, New York, to 15 years in prison for leading a loan modification scheme that defrauded distressed homeowners. Gotterup pleaded guilty on 16 June 2016 to conspiring to commit wire, mail and bank fraud. In addition, as part of the sentence, the Court ordered Gotterup to pay $2,500,050 in forfeiture. According to public filings, from 2008 to 2012, Gotterup and his co-conspirators made a series of false promises to convince more than 1,000 distressed homeowners seeking relief through government mortgage modification programs to pay thousands of dollars each in advance fees to numerous companies owned or controlled by Gotterup. Among other things, Gotterup directed telemarketers and salespeople to lie to distressed homeowner victims by telling them that they were "preapproved" for loan modifications and that they were retaining a "law firm" and an "attorney" who would complete their mortgage relief applications and negotiate with the banks to modify the terms of their mortgages. Contrary to these representations, Gotterup and his co-conspirators did little or no work in connection with these fraudulently induced advanced fees. Gotterup was arrested in October 2015 and has been incarcerated since then.

Goldman Sachs and the Big Short

Because the Federal Government stuffed TARP money into all the banks, SIGTARP was able to go in and investigate, looking back into deals that led to the banks running into trouble and requiring a bailout in the first place. One of their biggest targets was Goldman Sachs, Wall Street’s most successful firm. Their investigation there led to a Five billion dollar settlement over Goldman’s offloading of Residential Mortgage Backed Securities it knew were doomed to fail – a trade familiar to anyone who has seen the movies (or read the book) "The Big Short" and "Margin Call". One of the main criticisms levelled at SIGTARP is that the big beasts of Wall Street end up making (admittedly expensive) settlements, while the small fry from local banks go to jail. SIGTARP's justification is that the big beasts can afford big battalions of lawyers to fend off cases for years - a settlement inflicts some pain and some shame, and can get some big money back for the taxpayer quickly.

This is what SIGTARP’s boss Christine Goldsmith Romero said in a letter to Congress last month about the difficulty of prosecuting the big banks:

"While SIGTARP's investigations have resulted in the successful prosecution of CEOs and other top executives at medium sized banks and smaller banks, we have faced difficulties proving criminal intent of senior officials in large organisations that are designed to insulate high level officials from knowing about crime or civil fraud. In 2016, I proposed that Congress fix the problem of the "Insulated CEO" by requiring CEOs, CFOs, COOs and CCOs at the six largest Wall Street banks that took TARP dollars to sign an annual certification to law enforcement that they have conducted due diligence and can certify that there is no criminal conduct or civil fraud in their organisation. Until top officials have an affirmative duty to look for crime in their organisation, it is likely they will stay in the dark.

"This certification would give an incentive for CEOs to catch fraud in the company's business practices early and stop it, limiting damage. A false certification would give law enforcement a tool to prove criminal intent".

In the meantime it has gone in hard on Bank of America, JP Morgan Chase and Goldman Sachs - the latter making a $5bn settlement to stop the case in April of last year.

April 2016

The $5.06bn settlement with Goldman Sachs related to Goldman's conduct in the packaging, securitisation, marketing, sale and issuance of residential mortgage-backed securities (RMBS) between 2005 and 2007.

The resolution announced requires Goldman to pay $2.385bn in a civil penalty under the Financial Institutions Reform, Recovery and Enforcement Act (FIRREA) and also requires the bank to provide $1.8bn in other relief, including relief to underwater homeowners, distressed borrowers and affected communities, in the form of loan forgiveness and financing for affordable housing. Goldman will also pay $875m to resolve claims by other federal entities and state claims. Investors, including federally-insured financial institutions, suffered billions of dollars in losses from investing in RMBS issued and underwritten by Goldman between 2005 and 2007.

"Goldman took $10bn in TARP bailout funds knowing that it had fraudulently misrepresented to investors the quality of residential mortgages bundled into mortgage backed securities," said Ms Romero for TARP.

"Many of these toxic securities were traded in a taxpayer funded bailout program that was designed to unlock frozen credit markets during the crisis. This resolution holds Goldman Sachs accountable for its serious misconduct in falsely assuring investors that securities it sold were backed by sound mortgages, when it knew that they were full of mortgages that were likely to fail," said Acting Associate Attorney General Stuart F. Delery.

"This $5bn settlement includes a $1.8bn commitment to help repair the damage to homeowners and communities that Goldman acknowledges resulted from its conduct, and it makes clear that no institution may inflict this type of harm on investors and the American public without serious consequences."

A big fish in a small pond

In some of the banks SIGTARP investigated, the wrongdoing was committed by groups of employees. In other cases it was carried out by a dominant individual, often a larger than life chief executive who ran the institution like a personal fiefdom.

23 March 2016

On this day, Gilbert Lundstrom, CEO of the now-failed TierOne Bank was sentenced to 11 years in prison. CEO Lundstrom referred to TierOne as "his bank" when testifying--and that's exactly how he treated it. He was the architect of the bank’s aggressive and risky pre-crisis growth strategy. And when his risky moves backfired, he had a choice: tell the truth about TierOne’s millions of dollars in losses and limit the extent of further losses or take intricate steps to criminally conceal the bank’s true financial picture.

This bank CEO chose the latter - committing crimes, extending even more credit, and digging bank into an even deeper financial hole.

Lundstrom applied for $86m in TARP funds on behalf of the bank.

Make no mistake, this bank CEO was the driver of the criminal fraud. It was "his bank" and his fraud scheme.

Lundstrom falsified bank records, hid millions of dollars in losses, used old, inflated appraisals and altered board meeting minutes to conceal the bank's declining financial health.

He directed others to hide the bank's losses. During the trial, one employee testified that a colleague said that "Gil will kill me" if losses were reported.

CEO Lundstrom's fraud snowballed when he blatantly misrepresented bank losses to regulators and conspired with others to make false statements and representations through earnings reports, public statements, and regulatory examinations.

He even lied to shareholders that the bank had successfully applied for and later turned down TARP.

Fraud is not a victimless crime. A century old bank has been shuttered. Hundreds of employees lost their jobs. Shareholders that lost their investments include hardworking Americans whose retirement or children's education is now in jeopardy. And a community lost an important source of lending.

Profits from property

Another case dealt with a banker who was using the bank he ran to finance property deals he was a party to. This is a crime in America.

25 February 2016

A former TARP-recipient bank president was sentenced for his role in a bank fraud scheme in which he hid underperforming and at-risk loans from the bank and the Federal Deposit Insurance Corporation (FDIC), among others, announced Acting US Attorney G.F. Peterman, III of the Middle District of Georgia.

Gary Patton Hall Jr was sentenced by Senior US District Court Judge Hugh Lawson in Valdosta, Georgia to 84 months of imprisonment for conspiracy to commit bank fraud and conspiracy to commit fraud against the United States.

Hall was also ordered to pay restitution in the amount of $3,931,018 to the Federal Deposit Insurance Corporation (FDIC), as the successor in interest to the bank, and to the Small Business Administration and the US Department of Agriculture, as guarantors on fraudulent loans.

Hall entered a guilty plea to the charges on 4 December 2015.

According to facts stipulated in the plea agreement, Hall was the president and Chief Executive Officer of Tifton Banking Company (TBC) from August 2005 until June 2010. During that time, he was engaged in an ongoing scheme to mislead the bank and its loan committee about loans TBC made to local individuals and businesses.

As part of the scheme, Mr Hall hid past due loans from the FDIC and the TBC loan committee, which resulted in the bank continuing to approve and renew delinquent loans and loans for which the collateral was lacking.

Several of the borrowers eventually defaulted on the loans, resulting in millions of dollars in losses to TBC and others.

Hall admitted that in certain transactions in which he exercised approval authority, he hid his personal and business interests. In one instance, he approved loans to the buyer of a condominium in Panama City Beach, Florida, owned by himself. In doing so, he made false representations about the loans to TBC's loan committee and failed to disclose his personal interest in the transaction.

When the buyer’s loan payments became delinquent, Hall hid the loans from both the FDIC and state regulators. Hall received $50,000 profit from the sale of his condominium in this transaction, the entire purchase price being funded in full by an unsecured loan to the buyer approved by him. The buyer eventually declared bankruptcy resulting in a loss of more than $400,000 to TBC.

Additionally, Hall admitted to making fraudulent representations which led to loan guarantees being issued by the United States Small Business Administration and the United States Department of Agriculture on two other loan transactions. The loans were made by TBC, and guaranteed by the government agencies, to refinance earlier non-performing loans made by TBC.

Those guaranteed loans resulted in losses to the bank and the agencies of more than $2m. TBC was closed by the Georgia Department of Banking and Finance in November 2010 due to its poor financial condition. At that time, TBC had not repaid the $3.8m it received from the Department of Treasury’s Troubled Asset Relief Program (TARP).

But SIGTARP’s days are numbered. It was a temporary office, set up to police the TARP funding: when it comes to an end (in about five years time) so too does SIGTARP. The same was true of the Special Counsel set up to investigate the Savings and Loans Scandal of the 1990’s.

But insider frauds by banksters do not stop – they keep happening. Only the methods and the individuals change. That is why SIGTARP’s boss is now calling for the creation of a permanent Federal agency to investigate crimes by bankers.

"The threat of financial institution fraud is so serious and harmful as to require constant law enforcement expertise with dedicated resources. Financial institution fraud is typically committed in a series of criminal acts that incrementally evolve and grow more harmful over time - weakening our financial system from the inside. Without a dedicated permanent law enforcement office that evolves its knowledge and expertise as fraud evolves, more fraudulent schemes by insiders at financial institutions will grow undetected. Without a permanent paradigm shift, law enforcement will keep playing catch up, losing an opportunity to prevent fraud", said Goldsmith Romero in a letter to the US Congress.

The story of SIGTARP has a clear lesson for Irish lawmakers: if you want to punish bankers for wrongdoing, if you want to hold individuals to account, you have to prosecute them for offences specified as crimes in the law of the land. And to do that you need a specialist, dedicated police force that does nothing else but prosecute bankers. And you need to buy the crime-fighting software from SIGTARP.

Criminal Law and Police. With badges. And search warrants. And handcuffs. And guns.