Household net worth - the measure of the wealth owned by Irish people - has passed the pre-crisis peak, and now stands at its highest recorded level.

According to the Central Bank, the net worth of the Irish people stood at €726.8bn at the end of last year.

It increased by almost €15bn in the final quarter of 2017, with more than half of the increase coming from rising house values.

Net wealth is now the equivalent of €151,657 per person.

Net wealth is calculated by adding the total value of the housing stock and financial assets (such as savings and investments), and subtracting debt owed (liabilities).

The previous peak of €719.6bn was reached in the second quarter of 2007.

Wealth fell to a post-crisis low of €430bn in the second quarter of 2012.

Since then, it has risen by 69%, mainly due to the increasing value of the housing stock.

In the fourth quarter of 2017, the value of the housing stock increased by €8.5bn.

The Central Bank figures show that financial assets held by Irish households increased by €5.1bn. Liabilities declined by €1.2bn.

This gave an increase in net worth in the quarter of €14.8bn - an increase of 2.1%.

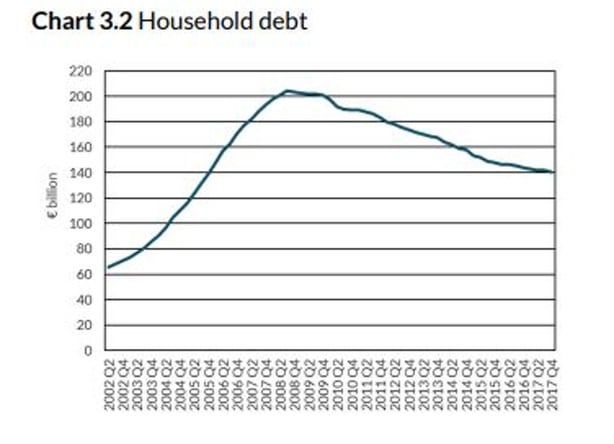

Household debt continued to fall, following the downward trend it has been on since 2008.

It ended the year at €140.5bn. This is the equivalent of a per capita debt of €29,307.

Household debt peaked at €204.2bn in the third quarter of 2008. Since then it has fallen by 31.2%, or almost €64bn.

Debt as a proportion of household assets is now 16%.

Debt as a proportion of disposable income fell by 2.5% to just under 137%, its lowest level since the start of 2004.

During 2017, household debt as a proportion of disposable income fell by over 10% - the biggest decline in the European Union. However, Irish households remain the fourth most heavily indebted in the EU.

Danish households are the most heavily indebted as a percentage of disposable income, followed by those in the Netherlands and Sweden.

Commenting on the Central Bank data, Goodbody's chief economist Dermot O'Leary said that while the aggregate data highlights the rebound in the Irish household position, the distribution of household assets and liabilities is vitally important.

He noted that Irish households in the 35-44 age cohort remain highly indebted, whereas younger generations have lower debt levels relative to the rest of the euro area.

He said this is where there will be signficant credit demand over the coming years.

"The older cohorts, where home-ownership rates are highest, have been the biggest beneficiaries of the boom in house prices over recent years.

"Separate work (Death & Taxes) we carried out earlier this week shows that one third of wealth is owned by those over 65, despite accounting for only 12% of the population.

"From a housing policy perspective, proposals around such issues and downsizing would surely help here," the economist added.