With the tracker mortgage scandal dominating the headlines this past week, much has been made of the support the banks got from the taxpayers for their previous bad behaviour in the form of the bailout.

And so, with excellent timing, the Central Bank has just released an economic letter updating the cost of that bailout.

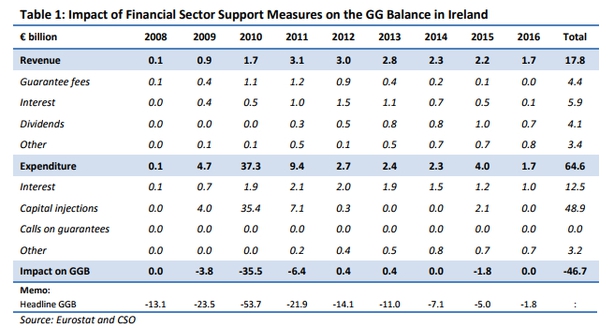

Let's get straight to the magic number. It's €46.7 billion. Or if you prefer, €46,700,000,000. Or if you prefer, 17% of 2016 GDP. Or if you really prefer, 24.7% of 2016 GNI*.

Any way you look at it, it's a big lump of money.

So what happened to the €64 billion that we usually hear was the cost of the bank bailout?

Indeed, it was the cost of the bailout - €64.6 billion to be precise.

But there has also been revenue – money earned by the State from the intervention.

This has come in the form of fees for the bank guarantee (now ended) interest on loans, dividends from bank shares, and other income.

Between 2008 and 2016, the total income from these sources has been €17.8 billion.

Interest has been the biggest component, at €5.9 billion.

Dividend income (€4.1 billion) is mostly profit the Central Bank has booked on its holding of State bonds issued to replace the Promissory Notes issued to bail out Anglo Irish Bank and Irish Nationwide.

This income will decline over time as the Central Bank unwinds its holding of these bonds.

Another factor reducing the €64 billion number is accountancy. To be more exact, there has been a reclassification of €15.1 billion of money – instead of calling it "capital transfers" – which worsen the deficit – that €15 billion has been reclassified as "financial transactions"; money that is expected to yield a reasonable rate of return.

Accordingly, these transactions do not have any impact on the General Government balance.

The other big spending category is interest, which accounts for higher spending directly attributable to the financial crisis-related borrowing.

The CSOI estimates that the State’s interest bill has been €12.5 billion higher since 2008 due to bailing out the banks. And this interest bill will continue to grow for years to come.

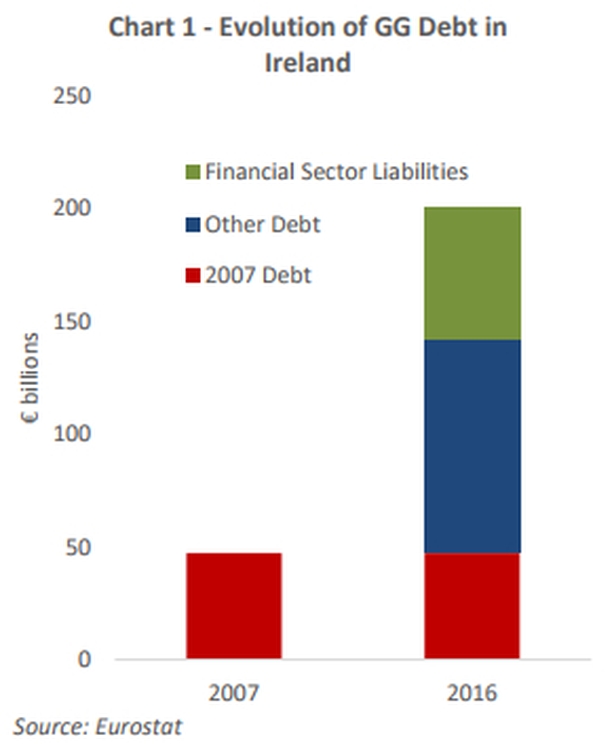

So what is the impact of all this on the General Government Balance – the debt we owe?.

According to the Central Bank staff (drawing on the filings made twice a year to Eurostat), financial support measures, as of the end of December 2016, have added €58.4 billion to overall General Government Debt.

This is 21.2% of GDP. Adjusting for the effect of multinational outflows (to see how it relates to the money available to the State to service this debt), and we see the banks have cost us 30.9% of GNI*.

This €58.4 billion compares to an overall increase in General Government Debt of €153.4 billion between 2008 and 2016.

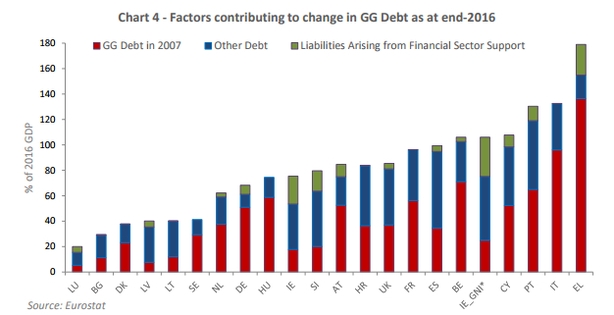

But we weren’t the only ones with a bank problem in 2008. Indeed 21 of the 28 EU states had to bail out their banks.

The net cost has been €218 billion (expenditure €412 billion, revenue €194 billion). But this cost has not been borne equally across countries.

As we know Greece and Ireland have paid the heaviest price. For the EU as a whole, the bank bailouts added 4% of GDP to debt. For Ireland the equivalent figure was 21% of GDP (or 31% of GNI*).

The bank bailouts did not cause all (or even most) of the increase of debt in EU states since 2008.

But it has left a very heavy legacy. The Average debt-to-GDP ratio in the EU is 84%, with ten states having debt ratios above 80% of GDP.

This compares to just three countries in 2007, when the EU debt ratio was 58%.

Using GNI*, Ireland’s debt ratio at the end of 2016 was over 100%.