The Irish Tax Institute says workers across all salary levels continue to pay more personal tax than they did ten years ago, despite a programme of personal tax reductions over the last seven years.

The professional body for tax advisors highlights the role of Universal Social Charge in driving increased progressivity in the income tax system.

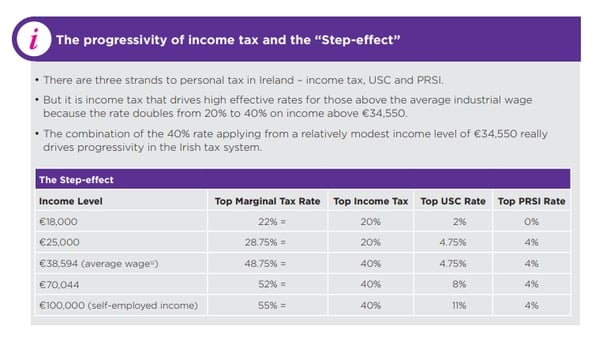

Progressivity means the more you earn, the more tax you pay - and Ireland's income tax system is recognised for being very progressive.

The institute says a single income earner on €35,000 is down 3% compared to their take-home pay in 2008, while a single worker on €120,000 takes home 9% less than a decade ago, that's just over €6,600.

The increased tax bill remains despite a series of changes to the tax system over the past seven years that include 20 changes to the USC.

The institute says USC has been central to driving progressivity, with reductions targeting lower and middle income earners balanced by increases for those earning above €70,000 a year.

They show this effect over time by comparing the USC paid by someone on €35,000 and someone earning €75,000.

When USC was first brought in, the person on €75,000 paid 2.6 times as much USC as the worker on €35,000, while today they pay 3.2 times as much.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

MORE ANALYSIS FROM SEAN WHELAN

Today's tax report shows that the more you earn the greater the percentage decrease in net pay.

The net pay of single income earners on €35,000 is down 3% or €964 compared to 2008 while those on €120,000 are down 9% or €6,679.

Families with two incomes of €35,000 are down 3% or €1,928 while families with two incomes of €75,000 are down 5% or €5,590.

The increased tax bills remain despite a programme of personal reductions over the past seven years that include three increases to the USC entry point, 11 USC rate reductions, six USC band widenings, two increases in the entry point into the Top Rate of income tax (40%) and a 1% decrease to that top rate.

However, the income tax reduction was not passed on to all taxpayers as a new 8% USC rate was introduced on PAYE income over €70,044 and a new 11% rate was introduced on self-employed income over €100,000.

The employee PRSI ceiling of €75,036 was also abolished during that period, increasing the PRSI bill for income earners over that salary level.

The impact on net pay as salaries rise reflects the highly progressive nature of Ireland’s personal tax system.

A comparison of the personal tax bill of workers at different salary levels over the past six years also shows the increasing progressivity in the Irish personal tax system.

The USC has been central in making it so.

The combination of USC reductions being targeted at lower to middle income earners and the introduction of a new 8% USC rate on earnings over €70,044 has driven progressivity.

In 2012, an individual on €75,000 paid 31.7 times the overall personal tax of someone earning €18,000. By 2018, this multiple has increased to 53.8.

An individual earning €100,000 paid 46.5 times the personal tax of a person on €18,000 in 2012. This has increased to almost 81 times the personal tax by 2018.

This highlights the increasing progressivity of Ireland’s personal tax system.

The big driver of the increasing level of progressivity between 2012 and 2018 is the USC.

In 2012, a person on €75,000 paid almost eight times the USC of someone on €18,000 and they now pay almost 17 times.

An individual earning €100,000 now pays almost 28 times (up from 11 times in 2012) the amount of USC of a person on €18,000.

Taking a salary level close to the average wage also highlights the role of the USC in progressivity.

A worker on €75,000 used to pay 2.6 times the USC of someone on €35,000 in 2012. That has now increased to 3.2 times.

A worker on €100,000 used to pay 3.6 times the USC of someone on €35,000 in 2012 and that has now increased to 5.3 times.

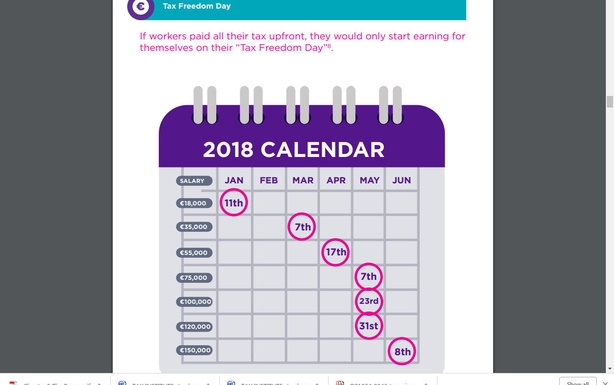

The Irish Tax Institute has also examined progressivity through the idea of a "Tax Freedom Day".

Taking the calendar year, the Institute calculates if workers paid their personal taxes to the Exchequer up front, on what date would they meet their tax obligations and then start earning for themselves.

The "Tax Freedom Day" calculation is another way of demonstrating how progressive the Irish personal tax system is.

Those workers on €18,000 meet their personal tax obligations to the State by 11 January, while workers on €35,000 work until 7 March before they earn for themselves.

Workers on €55,000 take until 17 April before they can count their earnings as their own and those on €75,000 take until 7 May before they are "tax free".

Those on €150,000 work until 8 June before their personal tax bill is paid and their earnings are their own.

Separate estimates of the average "Tax Freedom Day" for each EU state by Accountants EY for the Molinari institute in Paris show Ireland has the third earliest "Tax freedom day" in the EU - April 26.

Cyprus has the earliest, on March 27. For 14 of the 28 EU states "Tax Freedom Day" falls in June, while for a further seven, the day falls in July - including Germany (July 10) and bottom placed France (July 27).