Analysis: will the record amount of money currently on deposit in Irish banks give a post-pandemic boost to businesses and the domestic economy?

The news that deposits held by Irish residents reached a record €135 billion at the end of September has raised the possibility of a much-needed post-pandemic boost to businesses and the domestic economy. To understand where these savings will end up, it is necessary to understand why savings are so high, who is saving and why bank deposits might continue to grow?

Why are Irish savings so high?

High savings can be caused by an increase in investment, dissaving by other sectors of the economy such as government, or precautionary motives by savers fearful over an uncertain future. While bank deposits provide a good approximation of the amount of savings taking place, savings represent a type of residual, neither spent nor invested. Ultimately, investment drives demand and economic growth. Investment is financed through new money creation, such as the issuing of new loans and financing activities. In short, we shouldn't expect high savings levels to automatically translate into higher investment and economic growth.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

From RTÉ Radio 1's Today With Claire Byrne, Sharon Donnery, deputy governor of the Central Bank, on pandemic savings and spending

The mechanics of banks' balance sheets illustrate this. Under normal conditions, bank lending should be roughly equivalent to new deposits. A loan from a bank creates a new deposit. When a loan is repaid, deposits are reduced. The pandemic disrupted this process as banks become reluctant to issue new loans and instead increased their holdings of low yielding investment securities and government bonds. This is because a deposit (a liability on a bank’s balance sheet) must be covered by an equivalent asset. On the liability side of the banks’ balance sheet, a decline in consumption due to pandemic restrictions on the consumption of services alongside government policies to stabilise incomes meant that deposits continued to increase.

Who saved?

Aggregate rates of saving say very little about who actually saved. Although there is broad consensus across central banks that the increase in savings has been too large to be explained by the precautionary motive, not everyone saves. Savings tend to vary across countries and incomes. Before the pandemic, savings rates across many western economies had declined, but the savings of the top 1% had increased, leading to what has been described as a savings glut of the rich.

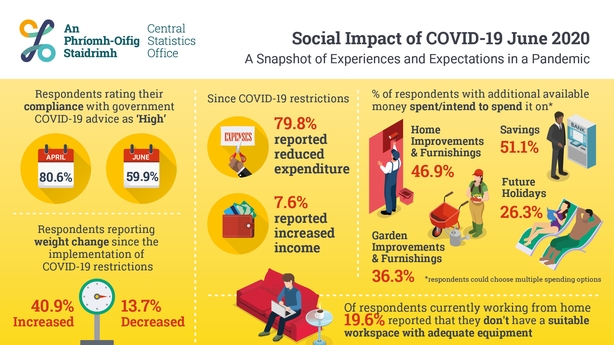

The large jump in Ireland's gross savings ratio in 2020 was driven by stable disposable incomes and a decline in consumption. A snapshot survey by the CSO in June 2020 indicated that 70% of respondents had experienced stable incomes, while 22% had experienced a decline, This suggested that the division between those who saved and did not save rested on the ability to continue remote working versus those who could not. More affluent households who were able to continue remote working would have been able to save comparatively more since many of the goods and services they typically consume were unavailable.

While Irish households on average increased their savings, the additional supports and investment taken on by the state implies that this went together with government dissaving.

Where will this cash go?

The Central Bank envisages that a rebound in consumption will bring the saving rate back to pre-pandemic levels by 2023. Survey data from the CSO suggests that very affluent households and those in rented accommodation intend to save the largest proportion of the pandemic savings boost. Less affluent households intend to spend savings on home improvements, furnishing and garden improvements. Not all businesses will benefit from this. Large international "super firms" are likely to capture a good deal of consumption by using their market power to mark up prices beyond the rise in input prices.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

From RTÉ Radio 1's News At One, Gill Stedman looks at how those lucky enough to have put money aside during their pandemic will use their savings

There are good reasons to believe that the level of deposits could continue to grow over the short term. Unlike in the aftermath of the banking crisis, Irish commercial banks currently have an excess of deposits over loans. But since banks do not lend out deposits, a return to normal lending will not see an immediate reduction in the level of deposits. Indeed, the CSO's snapshot survey suggests that over 50% of those with money put aside will continue to save.

Although the precautionary savings motive has been discounted as an explanation for the current level of deposits, households have good reason to be cautious. Rising energy costs have increased the cost of living, while the housing crisis has forced those in rented accommodation to save more. A significant portion of the costs of reducing emissions will also be borne by households. The retrofitting of homes is estimated to cost approximately €28 billion, much of which will be borne by households.

What could be done with this cash?

There is scope for creative policy thinking here. There are limits to what governments can do under a low interest environment to incentivise banks to reduce their levels of deposits. There is also little to be gained from another state savings saving scheme. Such an approach would largely benefit more affluent savers and would do little to improve the distribution of resources, address wealth inequality or meet the housing and climate investment needs of the economy. Negative interest rates could see Irish households continue to reduce their debt levels, which would see a reduction in deposits.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

From RTÉ Archives, RTÉ News report from 2001 on the new SSIA scheme to encourage saving

What government can do is create the incentives for productive investments in the areas of climate and housing and disincentivise the consumption of high emissions goods and services. Commercial banks could be incentivised to issue long term green bonds.

There is also scope for policy focused issuing of state-backed bonds using existing state agencies like NAMA and modelled along the lines of the land bonds used to fund tenant land purchases in the late 18th and early 19th century. These too were issued on the back of excess deposits in the banking system and their application today could represent a socially useful way of channelling savings to fund retrofits and the purchase and renovation of derelict buildings.

The views expressed here are those of the author and do not represent or reflect the views of RTÉ