All the chatter about the AIB flotation may well obscure the fact that banks are not the only financial institutions that can lend money.

With stunning originality, those other institutions are called non-bank lenders; and within the sector in The Netherlands something very interesting has been happening.

Since 2010, non-bank lenders there have seen a doubling of the amount of mortgage lending undertaken by Insurance Companies and Pension Funds (The ECB refers to this particular subset of non-banks as ICPFs, in a commendable effort to conserve pixels).

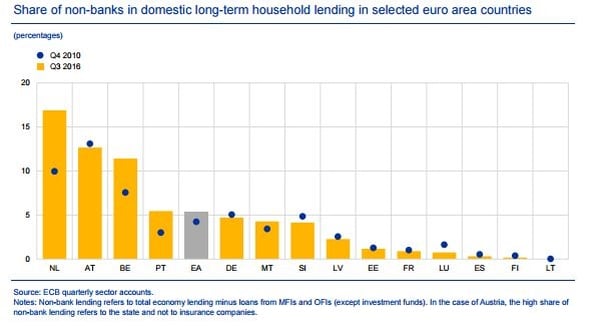

Across the Euro Area, the share of non-banks in long term lending to households has grown from 4.2% in 2010 to 5.4% last year. But in The Netherlands, Insurance Companies and Pension Funds currently finance 28% of new mortgages.

Historically the Dutch insurers have been active mortgage lenders. Mortgages account for 15% of Dutch insurers’ total assets, while they are 1.8% of Pension Funds’ assets. The more attractive mortgage yields have helped offset solvency pressures from the low interest rate environment.

The ECB thinks there is room for this share to grow, and "in principle, this also holds for other Euro Area ICPFs".

But there is no sign of a rush, particularly in Ireland.

There are 23 non-banks in the retail space here but only a couple - like Dilosk and Pepper - are involved in mortgages. Most of the others are in car finance and leasing. None of the Insurance Companies or Pension funds here sell mortgages.

But if the Dutch case is an example, they might well be able to add to the amount of money available for mortgage lending, keeping a lid on costs and spreading risk more widely (though the ECB accepts institutions may be reluctant to get involved in direct lending to consumers in markets where credit risk is higher: look at the Irish Non-Performing Loan level – around 14% compared to a Euro Area average of 5%).

The Dutch ICPFs sell mortgages both directly, through their own dedicated mortgage originators or banking subsidiaries, or indirectly through investments in mortgage funds. Over the period 2010 to 2016, their (non-securitised) mortgage lending went from €32bn to €73bn.

Most of this lending, as is usual in mainland Europe, is long term fixed rate, generally for more than 15 years.

As both banks and non-banks are covered by the same mortgage rules for loan to value and debt service to income ratios, the risk of the ICPFs gaining market share through "overly lax lending standards" is limited, according to the ECB in its latest Financial Stability Review.

As in other areas of investing, the push into mortgages has been driven by the search for yield. With interest rates at historically low levels, the Insurance Companies and Pension Funds can make a higher margin on mortgage lending, and with an attractive risk/return profile (most people tend to repay their home loans).

And given their long investment horizons, pension funds and Insurance companies actually have an advantage over banks when it comes to bearing the liquidity risk of investments in mortgage loans.

The ECB also says changes in regulation may be having an effect.

Under the EU insurance industry directive known as SOLVENCY 2, the capital requirements for an investment in a portfolio of non-securitised mortgage loans are lower than for an investment in a similar portfolio of securitised loans. This may explain the increasing interest of insurers in investing in direct mortgage loans rather than securitisation (which is bad news for Irish banks trying to securitize and sell off their mortgage books to get fresh funds for lending.)

The ECB also thinks stricter capital requirements for banks and uncertainty about future increase in risk weights for mortgages may have induced banks to reduce their mortgage lending.

The increased competition from the ICPFs in the mortgage market – particularly in The Netherlands and Belgium (where they have a share above 10%) , has implications for financial stability and macro-prudential policy, according to the watchdogs of Frankfurt.

In the short run, increased competition puts downward pressure on interest margins – good for consumers, but bad for banks, as it erodes their profitability. So far banks have been getting away with it because of increasing demand for loans with longer fixed rate periods (which are usually more profitable for the bank), but the ECB doesn’t think this happy situation will last for the banks.

Over the longer run, the ECB sees the rise of the ICPFs in mortgage lending as a good thing, contributing to a more diverse financial sector, with less maturity transformation and less leverage.

The ECB warns that the growth of non-bank lending could also see dangers rising, such as "an accumulation of credit risk for parties who are not equipped to manage or fully understand the risks they are exposed to".

Which surely means the non-banks are just like the banks.