The new Local Property Tax is to start on 1 July 2013, for the second half of the year.

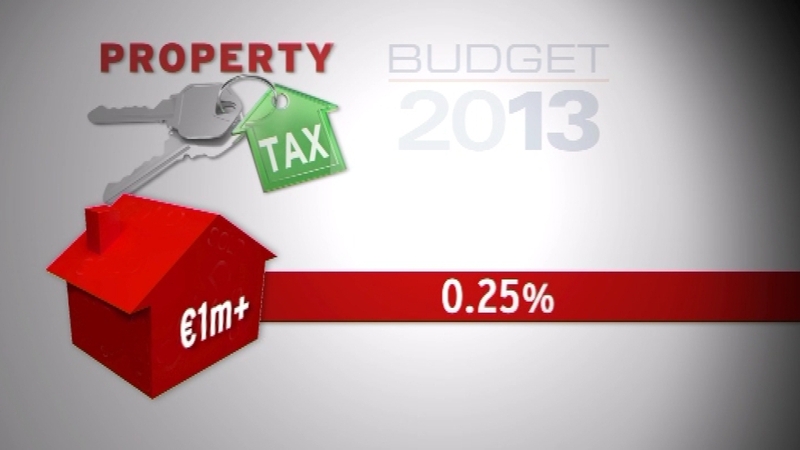

The rate of the tax will be 0.18% of market value up to €1m, and 0.25% on values above that level.

Finance Minister Michael Noonan said the rates will not be varied during the lifetime of the Government.

Explaining how the tax will work, he said that properties with a value of over €100,000 and less than €1m will be assessed at the mid-point of bands of €50,000.

For example, any properties valued between €150,001 and €200,000 will be assessed at 0.18% of €175,000.

Properties below €100,000 will be assessed at 0.18% of €50,000.

Properties valued at over €1m will be liable at 0.18% on the first €1m and 0.25% on the balance, with no banding applied.

The minister said that property owners will be able to choose from a wide range of payment options.

These will include payment by direct debit, cash payments, credit or debit cards, or deduction at source from salary or certain State payments.

There will be options to pay the charge in instalments.

Certain properties will be exempt from assessment and these will mainly correspond to exemptions from the household charge.

Mr Noonan said that from 1 January 2015, local authorities will have the power to vary the rates by 15% above or below the central national rates to better match their funding needs.