The International Monetary Fund has warned that debt-ridden banks were pushing the global financial system to the brink of meltdown and rich nations had so far failed to restore confidence.

The warning from IMF managing director Dominique Strauss-Kahn came as US President George Bush met finance ministers from the Group of Seven leading industrial nations at the White House

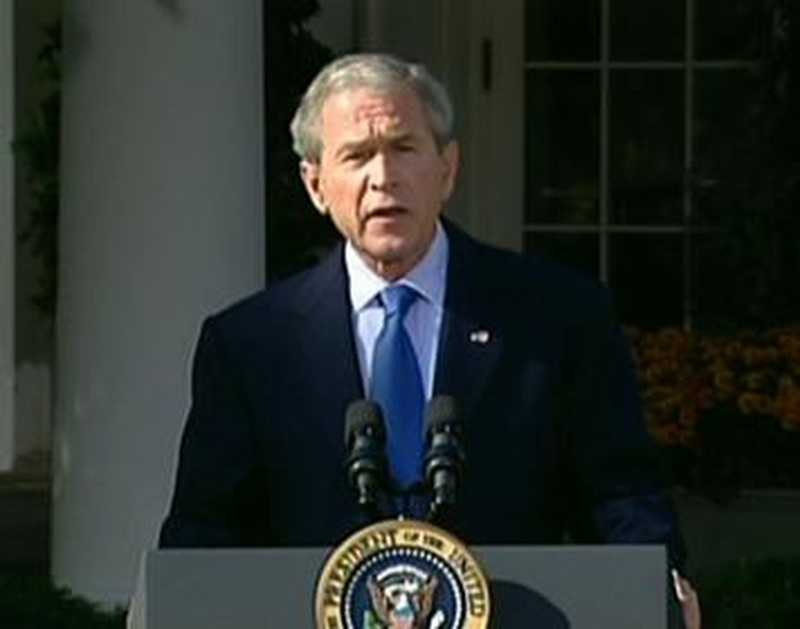

Speaking after the meeting, President Bush said that the governments of the world's richest countries must continue to work collaboratively to ensure their actions are co-ordinated in dealing with the ongoing crisis.

'All of us recognize that this is a serious global crisis and therefore requires a serious global response for the good of our people,' Mr Bush said in the White House Rose Garden after the meeting.

'The United States has a special role to play in leading the response to this crisis. That's why I convened this morning’s meeting here at the White House and it is why our government will continue using all the tools at our disposal to resolve this crisis,' he declared.

Mr Bush was joined by finance ministers from Britain, Canada, France, Germany, Italy, Japan, as well as the IMF chief, World Bank President Robert Zoellick and other officials.

With some warning that the crisis may be the worst since the Great Depression of the 1930s, Bush vowed no repeat of steps that deepened that crisis, such as enacting protectionist steps.

'There have been moments of crisis in the past when powerful nations turned their energies against each other, or sought to wall themselves off from the world,' said the US president.

'This time is different: the leaders gathered in Washington this weekend are all working towards the same goals,' he said. 'We're in this together, we'll come through it together.'

Mr Bush hailed international cooperation thus far, and said the G7 would work with an enlarged forum known as the Group of 20 that includes other major economies like China, India and Russia.

Meanwhile, the US government pushed to finalise a plan to buy direct stakes in banks as the International Monetary Fund warned markets could drop another 20% in a worst-case scenario.

Global stocks plunged to five-year lows yesterday as panic gripped, with the US S&P index and European stocks suffering their worst week ever, losing around a fifth of their value.

US Treasury Secretary Henry Paulson said the government would buy shares of financial institutions if necessary to halt market turmoil that has wiped out trillions of dollars of wealth and threatens to throw the global economy into major recession.

'We're going to do it as we can do it in a proper way that will be effective. Trust me, we're not wasting time, we're working around the clock,' Mr Paulson said late yesterday after the G7 meeting broke up.

He declined to discuss the size of the US bank equity purchases but said details were being developed quickly.

Leaders of euro zone countries will meet in Paris tomorrow in a new European attempt to coordinate action.