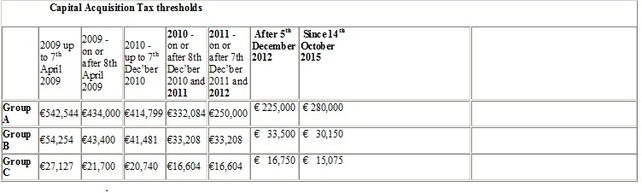

Gifts and inheritances can be received tax-free up to a certain amount. The tax-free amount, or threshold, varies depending on your relationship to the person giving the benefit. There are three different categories or groups. Each has a threshold that applies to the total benefits you have received in that category since 5 December 1991.

Group A applies where the beneficiary, the person receiving the benefit, is a child of the person giving it. This includes a stepchild or an adopted child.

It can also include a foster child if the foster child resided with and was under the care of the disponer and they provided the care, at their expense, for a period or periods totalling at least 5 years before the foster child reached the age of 18. This minimum period does not apply in the case of an inheritance taken on the date of death of the disponer. In this case the Group A threshold will apply provided that the foster child had been placed in the care of the disponer prior to that date.

Group A also applies to parents who take an inheritance from their child but only where the parent takes full and complete ownership of the inheritance. If a parent receives an inheritance where he or she does not have full and complete ownership of the benefit, or if a parent receives a gift, then Group B applies.

If a parent inherits from their child, and have full and complete ownership of the inheritance it is exempt from tax if, in the previous five years, the child took an inheritance or gift from either parent and it was not exempt from Capital Acquisitions Tax. In this case, no tax needs to be paid even if the inheritance from the child is over the threshold.

Group B applies where the beneficiary is the:

- parent (see also group A)

- grandparent

- grandchild or great-grandchild

- brother or sister

- or nephew or niece of the giver

If a grandchild is a minor (under 18 years of age) and takes a gift or inheritance from his or her grandparent Group A may apply if the grandchild's parent is deceased.

Group A may apply to a nephew or niece if he or she has worked in the business of the person giving the benefit for the previous five years and meets the following criteria:

- The nephew or niece must be a blood relation rather than a nephew or niece-in-law

- The gift or inheritance consists of property used in connection with the business, including farming, or of shares in the company.

- If the gift or inheritance consists of property then the nephew or niece must work more than 24 hours a week for the disponer at a place where the business is carried on, or for the company if the gift or inheritance is shares. But if the business is carried on exclusively by the disponer, their spouse and the nephew or niece then the requirement is that the nephew or niece work more than 15 hours a week.

- The relief does not apply if the benefit is taken under a discretionary trust.

Group C applies to any relationship not included in Group A or Group B.

If you receive a benefit from a relation of your deceased spouse, you can be assessed with the same group as your spouse would be if they were receiving the benefit from their relation. For example, if you receive a benefit from the father of your spouse, the group threshold would be Group C. But if you receive a benefit from the father of your spouse and your spouse is deceased, then the group threshold that applies to you would be the same as for a child receiving a benefit from a parent, Group A.

There is talk that these CAT thresholds will be increased at next October’s Budget. Currently the UK threshold is £325,000 – at 0.85p to the euro, works out at €382,352 or €102,352 of a disparity between our two countries. This may be the very yardstick the government will use to increase the Irish threshold.

You also may remember three years ago the government were going to introduce an incentive to give inheritances BEFORE you pass away rather than after – inheritances over the threshold given BEFORE death were going to attract the current rate of 33% while giving those surpluses over the threshold after death were going to attract the higher tax rate of 35%. While it never came to pass, it also may well be introduced next Budget.

John Lowe is a Fellow of the Institute of Bankers, founder and managing director of Providence Finance Services Limited trading as Money Doctor and regulated by the Central Bank of Ireland (www.independentfinancialadvice.ie ), plus author of the best-selling Money Doctor 2016: 100 Way to Save Cash For consultations and corporate seminars, call (01) 278 5555 or email jlowe@moneydoctor.ie Follow John on Twitter (@themoneydoc). Linkedin, Pinterest, Google+ & Facebook