Analysis: Lack of farming pensions and late retirement are preventing a new, younger generation from taking over farms and rural businesses

By Anne Kinsella, Teagasc

The sustainability of agriculture in Europe is intricately interwoven with the financial wellbeing of its farmers, particularly concerning retirement provision. Low pension coverage and late retirement are stalling what is known as 'generational renewal', which enables a new, younger generation to take over farms and rural businesses. As the farming population ages, ensuring adequate pension cover and the financial security of individual farmers becomes crucial in not only maintaining the vitality of rural communities, but in facilitating the broader dynamics of farm succession.

Recent research examined the design and implementation of some EU pension and retirement schemes. It identified gaps in Ireland’s current system and explored practical solutions for supporting Irish farmers through the retirement transition with learnings from other countries in Europe.

What retirement planning looks like for farmers

The Irish State pension was investigated in the context of the farming community, focusing on the first pillar system designed to deliver basic level pensions and alleviate poverty in old age. The findings illustrate the stark reality of how low-income farmers can fail to qualify either for the Contributory or Non-Contributory State Pension.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

From RTÉ Radio 1's Today with Claire Byrne, Anne Kinsella from Teagasc on how farmers need to plan for retirement with pensions and succession plans

Farmers face unique challenges regarding pension provision. These include lower and variable incomes, the intergenerational nature of farm ownership, cultural attitudes towards retirement and social capital aspects. A significantly higher proportion of the agricultural workforce are aged over 65 (25%) compared to the general population (4%). To compound the problem, a significant portion of farmers have limited pension coverage.

This is further exacerbated in that some may have 'gaps' in their Pay Related Social Insurance (PRSI) contributions. Such gaps can arise from late succession to farm ownership, or low-income years where contributions were not made. Income replacement rates in retirement are key in the decision to partly, fully, or indeed, never retire. Many farmers may need to continue working later in life or rely financially on family members, further hindering generational renewal.

What are the consequences of this pension gap?

Ireland lags behind our European counterparts in terms of its pension system and this has the potential to impact farmers negatively, resulting in poverty in old age. It creates a reluctance to retire and pass on the farm business. Reform is needed to ensure that the basic state pension is available to all engaged in farming, to protect their financial welfare and the financial welfare of their spouses/partners in retirement, thereby, facilitating full retirement.

Self-employed farmers predominantly begin their working life earlier and spend a longer time in employment than the employed

Recent EU pension reforms have improved pension security for the self-employed, but gaps continue to persist, so that the self-employed remain a vulnerable group. Overall, the self-employed in Ireland have lower levels of pension in comparison to those in employment - and self-employed farmers have the lowest pension cover of all, with many not planning to ever retire. Self-employed farmers predominantly begin their working life earlier and spend a longer time in employment than the employed.

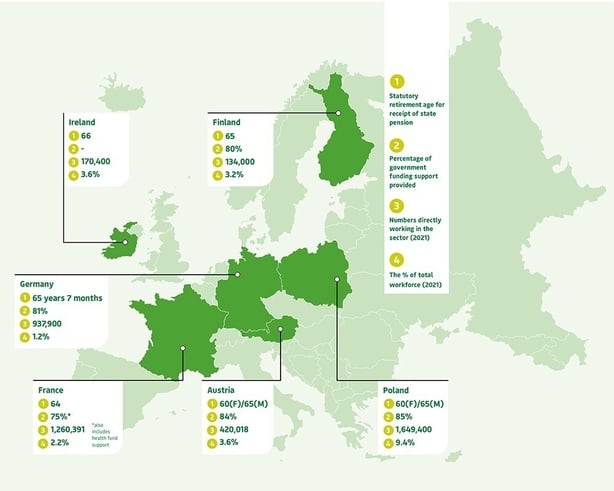

We evaluated pension systems for farmers in five European countries that serve as important benchmarks. All are members of the European Network of Agricultural Social Protection Systems (ENASP) that offer farmer tailored social welfare schemes. Each country has its own approach to farmer-specific social insurance, recognising farmers as a unique cohort.

In contrast, Ireland operates a single social security system with a general distinction between self-employed/employed workers, with farmers classified as self-employed. The ENASP countries recognise the unique needs of rural populations, including economic vulnerability, demographic challenges and the central role of family farms.

Research identified which aspects could be adapted to help increase pension coverage and improve retirement adequacy for Irish farmers. Analysis explored coverage levels, contribution models and qualification criteria. The findings highlight how policy reform could bring Ireland more in line with European norms.

Why we need a dedicated farm pension system

EU countries take two broad approaches: either farmers are included in the general self-employed social insurance system, or benefit from a dedicated preferential system. There are good reasons to adopt a separate model for farmers. Agriculture is a high-risk, low-profit sector and higher pension contributions may not be viable without support. Dedicated systems can also serve wider goals, like preventing rural depopulation, encouraging timely retirement, and promoting regional equality.

From RTÉ News, Aengus Cox reports on how attracting the next generation to farming has become a big issue given that the average age of Irish farmers is nearing 60

Drawing from the experience in ENASP countries, several key lessons emerge for improving pension provisions and facilitating generational renewal. The ENASP model could usefully be implemented in Ireland, where there are no specific state subsidies for farmers pensions.

Heavily subsidised state pension arrangements exist for farmers in France, Finland, Poland, Austria, and Germany. Subsidisation takes the form of reduced contribution levels, cover for all family farm labour and lower requirements in terms of contribution years. Levels of subsidisation ranges from 85% in Poland to 0% in Ireland.

The mandatory inclusion by ENASP countries of all farm workers provides a blueprint for ensuring that all workers have basic pension entitlement at a minimum.

READ: Why Irish farmers face big issues when it comes to pensions

The Irish and French systems require the highest level of pension contributions (40 years plus), while Austria and Germany only require 15 years of contributions. Finland requires no minimum contribution period. The Finnish model offering early retirement incentives shows how financial support can ease the path to retirement. It can boost private pension uptake by addressing affordability and trust barriers with financial planning support and education.

Corrective provisions to the current Irish system would ensure a minimum level of retirement income with consequent positive knock-on effects for succession or farm transfers. Making PRSI contributions mandatory ensures that entitlements are built from the start.

The Irish system, by not having mandatory registration for spouses or civil partners and "prescribed relatives" working on-farm, and by having a means-testing system has created significant gaps in pension coverage. This has consequent potential effects on poverty in old age and creates a reluctance to retire.

This creates difficulties for 'asset rich but cash poor' farmers

Provision of transitional supports assists farmers without adequate PRSI coverage to close the gap, and to ensure that those currently not covered do not remain disadvantaged.

While most countries apply some form of means-testing to determine the eligibility for pension top-up, Ireland applies a system of ‘imputation of notional income ’(attribute an estimated monetary income) to farmland and assets regardless of whether income actually arises, or how much arises. If title is retained to even a small landholding post-retirement, the imputation rules may mean a ‘fail’ in the means test.

This creates difficulties for ‘asset rich but cash poor’ farmers. Farmers ‘must’ therefore transfer land/assets to qualify, leaving them vulnerable to State and/or family and without any ‘nest egg’ to cover medical needs in old age. Farmers should be able to retain a small landholding without it affecting their pension entitlement.

Policy recommendations include the long-term retention of the ‘yearly average method’ as an optional method of calculating state pension entitlement where this results in a higher pension entitlement than the ‘total contributions approach’.

These reforms would require additional state subsidies, but such subsidies would reduce over time, as all farmers became included in the mandatory PRSI system. By adapting these strategies to Ireland’s context, policymakers can help secure the financial future of family farms, support rural vitality and promote meaningful generational renewal.

The author would like to acknowledge the work of her co-authors Dr. Michael Hayden, Dr. Bridget Mc Nally and Dr. Hana Hlochovo from Maynooth University for research undertaken for this project,

Follow RTÉ Brainstorm on WhatsApp and Instagram for more stories and updates

Anne Kinsella is a Senior Research Economist at the Rural Economy and Devlopment Programme at Teagasc

The views expressed here are those of the author and do not represent or reflect the views of RTÉ