Analysis: The state pension is now a mere part of a wider financialised portfolio, made up of other investments and private pension plans

By Conor Cashman and Margaret Buckley, UCC

Contemporary states are being challenged by rising pension costs and these costs seem to be fighting a losing battle in the face of demographic change, cost of living, and projected decrease in home ownership in later life. Moreover, debate and research about the costs and funding models of pensions are longstanding, with ongoing discussion about the role and place of the state pension. For example, recent analyses of what a decent standard of living looks like in retirement suggest that the state pension is, at best, viewed as a piece of the wider pension jigsaw made up of varying elements: the state provision, occupational pension schemes, private pension plans or combinations of them all.

From a social policy perspective, what does pension provision tell us about the nature of welfare provision generally, particularly in how people are expected to supplement the state pension? One insight comes from financialisation perspectives - the extent to which financial products (mortgages, debt, investments, and private pensions) play an increasing role in the day to day lives of citizens. When making provision for our retirement, we are expected to be active financial consumers and investors, making informed, crucial decisions about our pension investment portfolios.

The state pension is a mere element of a wider pension portfolio, made up of other investments and private pension plans, as we hope that the markets afford some luck to our future selves when the investment roulette wheel stops spinning at the end of our working lives. Arguably, a part of this financialised world is the upcoming pensions auto-enrolment scheme, creating an obligation (based on income and other criteria) for people to enrol in a pension plan if they have not done so already.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

From RTÉ Radio 1's News At One, new report says auto-enrolment could worsen pension inequality

The name 'auto-enrolment' might be relatively new, but the sentiment and mechanism behind it is not. British politician and future prime minister H.H. Asquith drew inspiration from Bismarckian Germany, where a programme introducing social insurance was embarked upon in the 1880s. This culminated in the Old Age and Disability Insurance Law of 1889, a ‘pay as you go’ system where each person was responsible for providing for old age instead of shifting this burden on to future generations. It was funded by contributions from employee, employer and state.

While Chancellor of the Exchequer, Asquith had managed to accumulate enough money through income tax reforms to fund what would become the non-contributory Old Age Pension Scheme for the UK and Ireland. The Old Age Pension Act 1908 is regarded as one of the first of the modern welfare state. The ‘People’s Budget’ was announced by Asquith in December 1908, just prior to the Old Age Pension being rolled out. It was announced both as a budget which would reflect the new liberal policy agenda, which focussed more on social problems. The majority of politicians from all ideologies recognised that it was a good, and necessary, measure to address the problem of the aged poor.

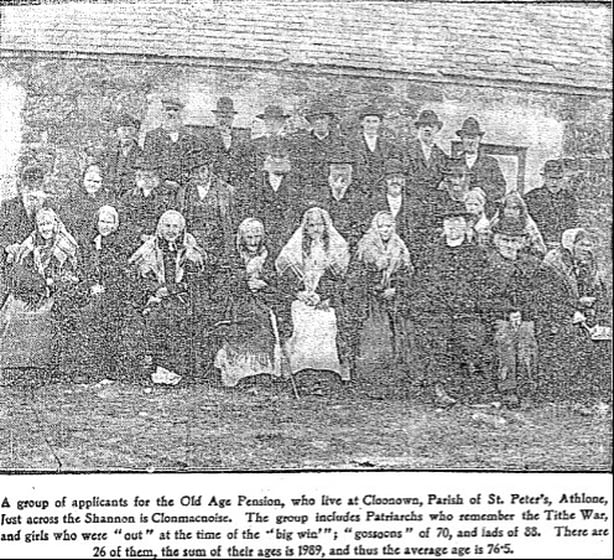

Asquith stressed that the amount of money to be provided by the pension was designed not to be enough to live on, but to be enough to supplement income and to encourage saving earlier in life. The initial act allowed for payment of 5s per week and 7s 6d for married couples. The disqualifications included being 'a pauper, a criminal, having a lack of temperance and habitual unemployment'. Accordingly, the people most in need of the pension (the poor and unemployed) could be disqualified because of their need until 1911. The Old Age Pension Act of 1911 allowed for a universal pension for everybody over the age of 70.

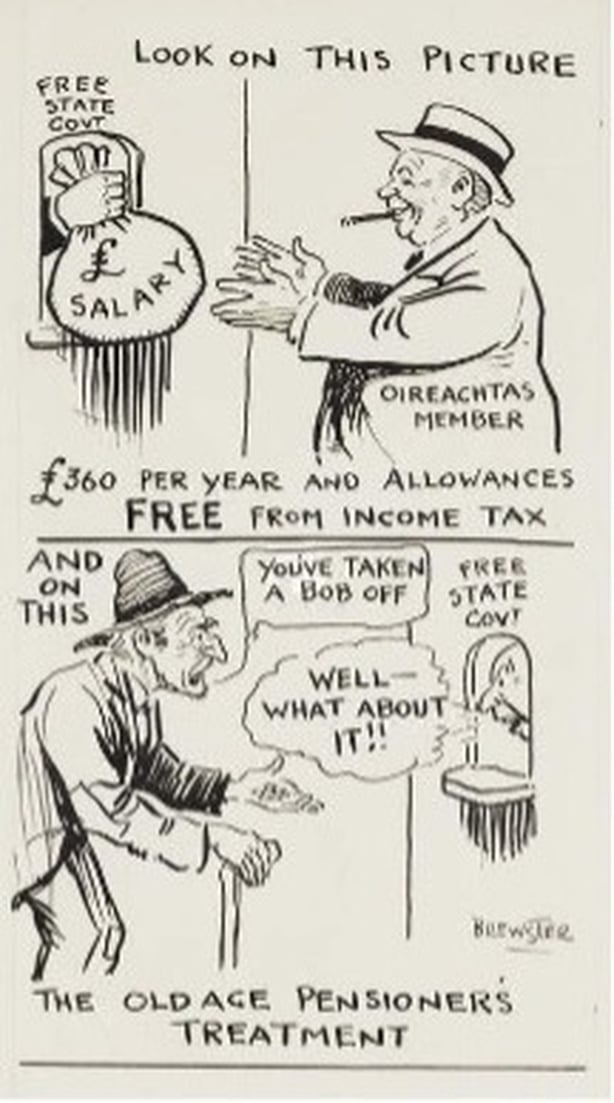

Infamously, owing to the financial struggle facing the Irish Free State after Independence, one of the first cuts in public spending was to the old age pension. In 1924, Minister for Finance Ernest Blythe proposed to reduce the pension by 1s (10%) per week. The reduction was justified in the Dáil on the basis that if taxation were increased instead, the old age pensioners 'would not be saved from hardship' because it was envisaged that an increase in taxation would result in an increase in the cost of living and increased unemployment.

How far have we come since the 19th century? The state pension continues to be a part of how many people will meet their future income in retirement. The nature of policy, it seems, continues to follow Asquith's approach regarding the state pension being a supplement to income and savings. However, we are enrolled, encouraged and urged to become financialised citizens today, investing in the pensions market to supplement the state pension.

Many questions will arise about different people's starting positions in the financialised, auto-enrolment pensions world - from the impact of precarious contracts, to the differing levels of workforce participation depending on age and gender, to financial literacy levels. Auto-enrolment is a clear sign that, whatever other decisions governments make about retirement and the role of the state pension, citizens are playing an increasingly financialised pensions investment game. To draw on a game analogy, not all of us will be starting from the same square marked 'GO!’.

Dr Conor Cashman and Dr Margaret Buckley are lecturers in social policy in the School of Applied Social Studies in University College Cork. They are former Research Ireland awardees.

Follow RTÉ Brainstorm on WhatsApp and Instagram for more stories and updates

The views expressed here are those of the author and do not represent or reflect the views of RTÉ