New figures from the Central Bank show that the average interest rate on new mortgages here eased to 3.53% at the end of November, down three basis points from the previous month and the lowest level since February 2023.

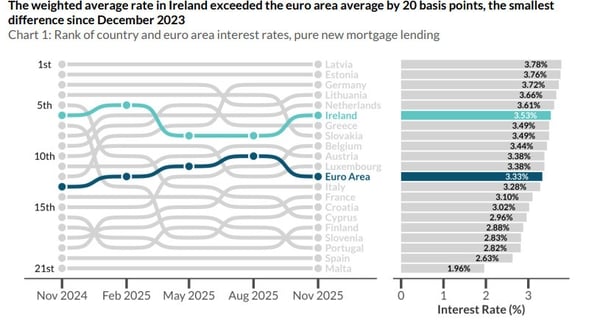

The Central Bank said the euro area equivalent was 3.33%, which made Irish mortgage rates the sixth highest in the euro zone, unchanged from October and the smallest difference since December 2023.

Today's figures show that Latvia had the highest mortgage rate at 3.78% in November, followed by Estonia (3.76%) and Germany (3.72%). Malta had the lowest rate at 1.96%, with Spain at 2.63% and Portugal at 2.82%.

According to the Central Bank, the average interest rate on new fixed rate mortgage agreements, which make up 89% of the volume of new mortgages, was 3.46% in November, down three basis points from the previous month and down 33 basis points from November 2024.

Meanwhile, the average interest rate on new variable rate mortgage agreements was 4.08% in November, nine basis points down from October and 33 basis points lower in annual terms.

The total volume of pure new mortgage agreements amounted to €1.1 billion in November, €59m or 6% higher on November 2024.

Ross Lynch, Senior Mortgage Advisor with NFP Ireland, said that Irish mortgage rates are now at their lowest level since February 2023, and this, combined with the fall in the average interest rate on new mortgages, will be welcome news to would-be house buyers.

Mr Lynch said that as euro zone inflation appears to be under control and the bloc's economy is showing resilience, it is looking unlikely that there will be any more ECB rate cuts over the coming months.

"This could put the brakes on any further falls in average Irish mortgage costs in the near future," he stated.

He said that regardless of what happens with ECB rates, however, a step up in competition amongst lenders has seen better rates emerge in recent months.

"So first-time buyers should be sure to shop around for their mortgage while existing mortgage holders should investigate if they can get a cheaper mortgage deal. Switching activity is back on the rise, and many borrowers, particularly those on standard variable rates, could stand to save hundreds or even thousands per year by reviewing their current deal," he said.

"You may not even have to switch lender to get a better deal. You may qualify for a cheaper mortgage as a result of having a much loan-to-value (LTV) than when you first bought your home. Now is an ideal time to seek out advice and explore options," he advised.