The latest Office Review and Outlook Report from independent property firm HWBC shows that after a slow start, the Dublin office market staged a recovery in 2024 with annual take-up reaching 2.15 million square feet.

HWBC said this marked a 63% increase on 2023 figures and was closer to the long-term average for the market of 2.5 million square feet.

With over 1.2 million square feet of office space already reserved, including high-profile developments such as Marlet's College Square, the property agency forecasts a similar strong outcome for 2025 to that recorded in 2024.

HWBC said the recovery seen in Dublin's office market last year was driven by pent-up demand from the financial, professional services and technology sectors.

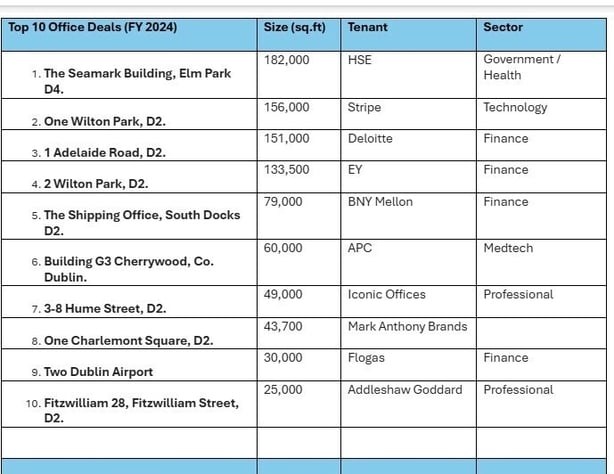

It noted that seven transactions exceeded 50,000 square feet with four of these over 100,000 square feet including Stripe's 156,000 square feet and EY's 133,000 square feet at Wilton Park.

New completions also reached 1.99 million square feet, with 60% pre-committed on delivery, underscoring strong occupier confidence in return office trends.

HWBC predicts corporate demand for BER A-rated space in Dublin 2 and Dublin 4 will drive increased competition among would-be occupiers and reduce supply over the next 12 months.

There is about 1.55 million square feet of A-rated standing stock over 20,000 square feet available in Dublin 2/4, equating to less than two years of supply at current demand levels.

With no speculative space under construction for completion beyond 2027, the market faces an impending shortage of new high-quality stock, HWBC cautions.

The report today says that about 1.57 million square feet of new office space is currently under construction in Dublin with around 79% of this reserved for companies such as KPMG, Citi, Deloitte and Google.

HWBC estimates 675,000 square feet is due to complete this year including the Treasury Annex for Google, 2 Grand Canal Quay and The Frame on Baggot Street.

Meanwhile, sustainability continues to influence corporate leasing decisions, HWBC says, with a "green premium" driving demand for BER A-rated space and environmentally certified spaces.

Today's report finds that multinational firms are increasingly prioritising city locations to entice employees back to the office. This trend saw over one million square feet of take-up in Dublin 2/4 last year, with all occupiers of scale choosing A rated space.

The suburban market, which accounted for 25% of take-up in 2024, is expected to see steady activity in 2025, HWBC predicts, as price-sensitive occupiers broaden their searches beyond the city centre.

Sandyford, Cherrywood, and Dublin Airport remain key suburban hubs.

While the outlook is optimistic, HWBC noted potential headwinds from the international market, particularly concerning US corporates navigating the policy environment under the second President Donald Trump administration.

It said this could lead to delays in decision-making for some occupiers, though strong fundamentals in the Dublin market are expected to offset these uncertainties.

Iain Sayer, Managing Director of HWBC, said the Dublin office market continues to demonstrate resilience and adaptability, driven by strong corporate demand for top-tier, city-centre space.

"Sustainability has moved to the forefront of occupier priorities, and this will shape the market for years to come," Mr Sayer noted.

He said the company's outlook for 2025 is one of cautious optimism.

"While we anticipate leasing activity in the 2-2.5 million square feet range, the market is becoming increasingly divided," he said.

"Demand for older, less sustainable stock continues to weaken, which is creating a drag on overall vacancy rates, but the prime end of the market is thriving. The ongoing push for environmentally certified, A-rated buildings will lead to a more competitive landscape for occupiers, particularly in the Central Business District, where supply is already tight," he concluded.