If the Covid-19 pandemic taught us anything, it is how dirty cash really is.

Banks in China started disinfecting money, while many businesses simply stopped accepting cash in an effort to curb the spread of the disease.

As we tried to keep the germs at bay, the boom in contactless payments took off.

Whether we like it or not, this in turn changed how we pay for things right across the world.

We've been taking a look at the best ways to pay while travelling abroad, and how to reduce or even avoid foreign exchange fees.

Is cash no longer king?

A number of countries around the world are striving to become cashless.

Sweden, Brazil and China are among a handful that are already well on their way.

So if you're travelling to these countries, you'll probably find very little need for cash - if any.

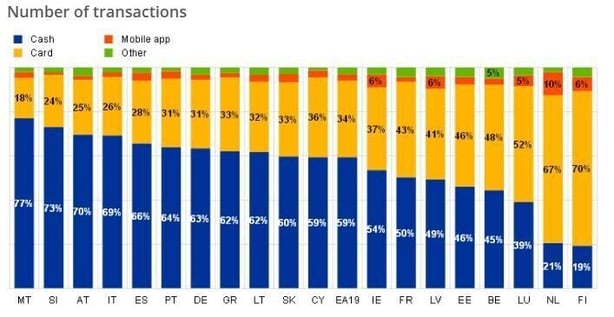

But cash is still the most frequently used payment method across the euro area.

Just four countries bucked this trend last year, according to figures from the European Central Bank.

Finland, the Netherlands, Luxembourg and Belgium used card more than cash.

Malta, Slovenia, Austria and Italy are among the EU countries that still very much favour cash.

Last year, 59% of all transactions across the euro area were carried out using cash, down from 72% three years earlier.

How much cash you bring on holidays will very much depend on where you're travelling and the activities you have planned.

No matter where you're travelling to, tips and taxis are probably the two main reasons you'll need cash.

What about Revolut and N26?

"I'll Revolut you," is a phrase most of us have become accustomed to.

Whether you're splitting a restaurant bill or just paying for a coffee, Revolut and fellow digital bank N26 are growing in popularity right across the world.

Apart from allowing you to make quick payments and transfers, they'll also help you avoid fees when travelling outside of Europe.

If you have a free account with Revolut, Darragh Cassidy of price comparison website Bonkers.ie said you won't be charged any foreign exchange fees on purchases up to a total of €1,000 a month. After that, a small fee applies.

With N26, there is no purchase limit.

"Both providers will also give you a better exchange rate than you'd get with any of the main Irish banks," Mr Cassidy said.

"So I’d definitely recommend using one of these providers if travelling outside the eurozone.

"And of course they’ll also help you easily keep track of what you’re spending," he added.

Should I use my credit and debit cards?

If you have a credit or debit card with a traditional bank you may be charged fees when travelling abroad, depending on whether you have a Visa or Mastercard, and the country you're using your card in.

If you pay by debit card, Mr Cassidy said you'll be charged a minimum fee on every transaction by some providers.

"As a result, you should avoid using your debit card to make lots of small transactions as your fees could balloon," he suggested.

"On the flip side, most debit card providers cap charges at a maximum of around €11 or €12 per transaction, which makes debit cards good for very large purchases," he added.

When it comes to credit cards, banks don't generally charge a minimum fee, but they also generally do not cap charges on a single transaction.

"This means if you splurge on a €2,000 laptop in the States for example you could be hit with a fee of up €50 or more depending on your credit card and your bank," Mr Cassidy explained.

And so, he suggests using your credit card, Revolut or N26 for smaller purchases, and your debit card for larger purchases of around €500 or more.

Should I pay in the local currency when using card?

Quite often when you go to pay for something in a non-eurozone country you will be offered the choice to pay in euro instead of the local currency.

The idea is that you can lock in a guaranteed price for your purchase at the till and not have to worry about the exchange rate.

But this might not be the best option.

Mr Cassidy said that price you're locking in will usually be worse than the price you would be charged in a day or so when your bank processes the transaction.

"Always decline the offer to pay in euro and pay in the local currency instead - especially if you have Revolut or N26," Mr Cassidy suggested.

Should I stay away from ATMs abroad?

ATM fees are extremely common, and can be extremely high.

Quite often ATMs in areas like pubs, nightclubs, forecourts and airports hike up their fees.

Some of these fees can be up to 10% of the amount withdrawn or more, Mr Cassidy warned.

On top of this, if you're travelling outside the eurozone, you’ll be hit with foreign exchange fees.

Mr Cassidy said these can be up to 3.5% of the amount withdrawn and a minimum charge of over €3 usually applies.

"So withdrawing €50 could potentially cost you close to €10 in a worst case scenario," he said.

"Because of the minimum fee, you shouldn’t be withdrawing small amounts of cash," he added.

If you want to take out cash, try to do so before leaving home - and keep it somewhere safe.