New figures from Kantar show that grocery price inflation rose again in recent weeks and now stands at 16.8%, up from 16.4%.

Kantar said its latest figures show that although value sales are up significantly, grocery price inflation is still the driving factor rather than just increased spending.

It cautioned that consumers' annual grocery bills are set to rise by €1,211 if they do not make changes to their shopping habits.

Kantar said that take-home grocery sales in the four weeks to March 19 increased on the back of a month of celebrations including Mother's Day, St Patrick's Day and the Irish rugby team winning the Six Nations Grand Slam.

Value grocery sales increased by 13.3%, up from 10.2% in February, as the average price per pack increased by 13.8%.

Visits to supermarkets were up 13% year-on-year - the highest level of footfall since March 2020. In actual terms this means shoppers made two additional trips to stores in March, Kantar said.

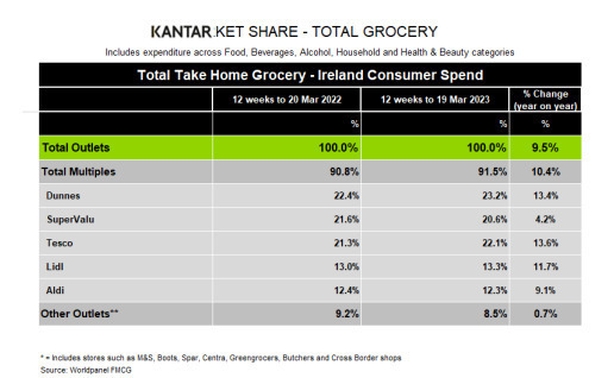

In the 12 weeks to March 19, take-home grocery sales increased by 9.5% as they contributed an additional €268m to the overall market performance.

"Consumers are opting to shop little and often to help manage their household budgets. Basket mission really drives growth for the overall market - up 25.1% - with shoppers spending an additional €119.6m year-on-year," Emer Healy, Senior Retail Analyst at Kantar, said.

We need your consent to load this rte-player contentWe use rte-player to manage extra content that can set cookies on your device and collect data about your activity. Please review their details and accept them to load the content.Manage Preferences

The "indulgent" mission grew 17.7% year-on-year, as shoppers made more indulgent trips in line with the festivities in March, Ms Healy added.

Meanwhile, the Irish market continues to see much stronger own label growth (13.5%) than brands (6.2%) as shoppers look for ways to save money.

Value own label brands saw the strongest growth of 34.5% on an annual basis with shoppers spending €18m more on these ranges.

Own label now holds a higher value share than brands - 47.3% compared to 47% - Kantar noted.

Online sales also remained strong over the 12-week period, up 2.6%, with shoppers spending an additional €3.9m online year-on-year. More frequent trips (4%) and higher average prices (15.5%)

helped to drive growth in the latest period under review.

Dunnes continues to hold the highest share amongst all retailers at 23.2%, with growth of 13.4% year-on-year. Kantar said its growth is as a result of an influx of new shoppers to the store, up 1.3 percentage points, and shoppers returning more often to store, up 4.7%.

Tesco holds 22.1% of the market with growth of 13.6% year-on-year, and the strongest frequency growth amongst all retailers, up 12.8%.

SuperValu holds 20.6% of the market and growth of 4.2%, with shoppers making the most trips in store

when compared to all retailers, with an average of 21.7 trips over the 12-week period, an increase of

12.1% year-on-year.

Meanwhile Lidl holds 13.3% share and growth of 11.7% year-on-year. An influx of new shoppers and more frequent trips contributed an additional €25.2m to overall performance.

Aldi holds 12.3% share with growth of 9.1% year-on-year, welcoming a boost in new shoppers and more frequent trips contributed an additional €40.1m to overall performance.