Irish homeowners continue to pay above average rates for their mortgages, the latest figures from the Central Bank show.

At 2.72% in September, the average interest rate on a new mortgage in Ireland has fallen by 0.02% compared to August and by 0.06% compared to September of last year.

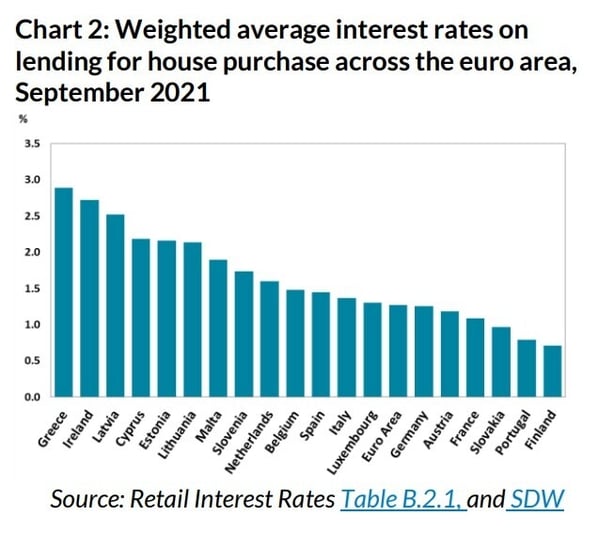

But Irish mortgage rates are still the second-highest in the euro zone and are over double the currency bloc's average of 1.27%.

Greece, at 2.89%, has the highest rates once again this month, while Finland has the lowest average rate in the euro zone at just 0.71%, closely followed by Portugal at 0.79%.

Figures from Banking and Payments Federation Ireland show that the average first-time buyer mortgage in Ireland is around €250,000.

This means someone borrowing this amount over 30 years is paying almost €180 extra a month, or almost €2,200 a year, compared to our European neighbours.

Daragh Cassidy, Head of Communications at bonkers.ie, said the fall in mortgage rates over the past year is obviously welcome and the overall trend is downward - albeit very, very slowly.

He said that despite the impending exits of both Ulster Bank and KBC Bank Ireland from the Irish market, competition in the mortgage market is relatively strong with ICS mortgages, EBS, Finance Ireland and Avant Money all reducing rates over recent months.

"However this isn't really feeding through to the average rate consumers are being charged just yet. This is partly because many of the lowest rates in Ireland right now come with big caveats - such as a 40% deposit or are only available on B+ energy rated homes - something which is beyond the capabilities of many first-time buyers," Mr Cassidy said.

He also noted that the bigger players like Bank of Ireland and Permanent TSB in particular, which have a large share of the mortgage market, charge among the highest rates.

He urged first-time buyers to make sure they do their research, shop around and consider all mortgage lenders.

He also encouraged mortgage holders to consider switching to a new mortgage provider.

"Switching activity has been growing strongly in recent months, which is great to see. In September, over 600 people switched their mortgage, which was up almost 37% year-on-year according to the BPFI," Mr Cassidy stated.

"While there are costs associated with switching mortgage provider, in some cases banks will provide a sizeable cashback incentive to those who switch," he added.