More than half of the value of Tullow Oil was wiped out today as chief executive Paul McDade stepped down.

The Africa-focused oil producer also scrapped its dividend after failing to meet production targets due to weak performance by flagship assets in Ghana.

Tullow has been plagued by technical problems at its Jubilee field in Ghana and a delay in completing a well at the TEN offshore field.

Tullow, which had already cut its output estimates by 14% this year to 87,000 barrels per day (bpd), said its 2020 output would shrink further to a maximum of 80,000 bpd and fall again to around 70,000 bpd in 2021-2023.

Tullow also suffered blows in recent months due to setbacks at East Africa projects in Uganda and Kenya where it is yet to reach final investment decisions.

It also saw a setback to its plans to develop oil fields in Guyana, one of the world's hotbeds for exploration, where oil it discovered was of a lesser quality than hoped.

"The board has been disappointed by the performance of Tullow's business and now needs time to complete its thorough review of operations," Executive Chairman Dorothy Thompson said in a statement.

Tullow's director for exploration, Angus McCoss, also resigned today.

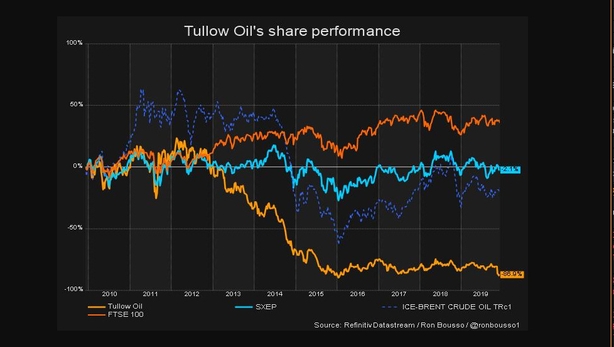

Its shares were down over 70% today, the company's biggest daily loss since 2004.

In a conference call, the company said it was open to receiving offers to acquire the company at the proper value.

The Africa-focused oil firm also suspended its dividend, which it only reinstated this year after a hiatus since 2015, as it still focuses on reducing its debt pile.

Tullow, which had a market cap of around $2.6 billion after the slump in its share today, expects it net debt to stand at around $2.8 billion at the end of this year, and $2.6 billion at the end of 2020.

It did not change overall reserves estimates for its portfolio. Such downgrades can impact oil producers' credit lines. Shares in Tullow's partner in Ghana, Kosmos Energy, fell around 8.5%.

Free cash flow is expected to come in at a minimum of $150m next year at an oil price of $60 a barrel, less than half of this year's expected $350m.

The group also slashed its capital expenditure programme and cut costs at its operating fields.

Tullow has $300m in debt due in 2021 and a further $650m in 2022.

Tullow's chief financial officer, Les Wood, said today that the group was "comfortable" with its covenants with banks.

He added he expected its debt to EBITDA, or core profit, ratio to stand at 1.8 to 2 times at the end of this year.

Cantor Fitzgerald Europe described the difficulties the company announced as "a bit of a kitchen sinking".

"Investors may well agree that a reset is the correct approach, although that is unlikely to prevent another huge sell-off today," the financial services company said in a note.