Wells Fargo & Co today reported a 26% slump in quarterly profit, as mortgage income sank and it braced for additional legal expenses tied to a sales practices scandal that erupted more than three years ago.

The bank is operating under heavy regulatory scrutiny, including an unprecedented cap on its balance sheet by the Federal Reserve.

It is still trying to rebuild its reputation after revealing in 2016 that it had opened potentially millions of unauthorised accounts.

The bank has paid billions of dollars in fines and penalties and launched a campaign to win back the faith of its customers and investors.

It said today it had set aside $1.6 billion for legal expenses related to the retail sales practices.

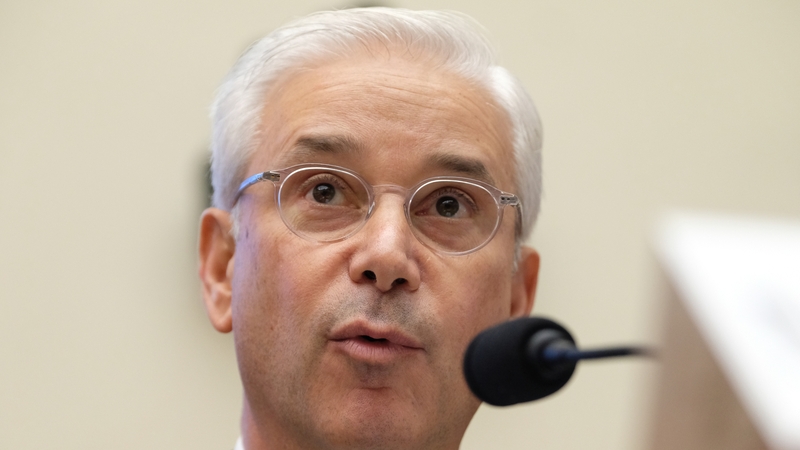

The San Francisco-based lender last month appointed Charles Scharf, a one-time Jamie Dimon protégé known on Wall Street as a detail-oriented number cruncher who excels in streamlining operations, as its new top boss.

It said its net interest income fell 7.5% to $11.63 billion as the US Federal Reserve lowered borrowing costs for consumers twice in the quarter to sustain the more than decade-long economic expansion.

Its mortgage income fell 45%, even as US refinancing activity more than doubled from a year ago, according to data released by the Mortgage Bankers Association last week.

Provision for credit losses rose 20% to $695m in the third quarter from a year earlier.

It said its net income applicable to common stock fell to $4.04 billion, or 92 cents per share, in the third quarter ended September 30, from $5.45 billion, or $1.13 per share, a year earlier.

Excluding items, the lender earned $1.07 per share, compared to analysts expectations of $1.15, according to IBES data from Refinitiv.