The Central Bank has issued its "most serious possible outcome to a fitness and probity investigation" to Anne Butterly, the former manager of Rush Credit Union.

The notice prohibits Ms Butterly from carrying out any controlled functions in any regulated financial service provider for an indefinite period.

This preludes her from carrying out any management or advisory roles in the sector.

This follows a Central Bank investigation into Ms Butterly's involvement in unauthorised transactions on accounts at Rush Credit Union.

Last November, the High Court appointed liquidators to Rush Credit Union following an application by the Central Bank after investigations had revealed significant misappropriation of funds.

A number of governance, financial and internal control failures were identified at Rush Credit Union.

Deficiencies uncovered included control of bank and cash, lending practices, as well as the day-to-day running of the credit union.

Rush's August management accounts show liabilities exceeded total assets by €1.2m, with alleged misappropriation of €800,000 bringing this figure to €2m.

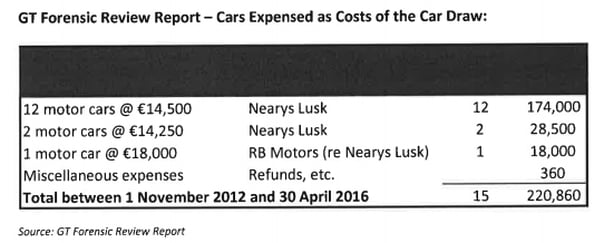

The credit union spent €220,860 on 15 car draws between November 2012 and April of last year, however, the Central Bank said a report was "unable to locate details winners of previous car draws".

In a statement today, the Central Bank said its investigation into Ms Butterly has now concluded with the issue of a prohibition order of indefinite duration.

The bank said this was the "most serious possible outcome to a fitness and probity investigation".

"This outcome shows that that the Central Bank’s regulatory reach extends to individuals, and not just to firms," commented the Central Bank's Head of Enforcement Investigations Brenda O'Neill.

"We take individual accountability very seriously and this case demonstrates our resolve to act where an individual’s conduct falls below expected standards," she added.

Ms O'Neill said that through its supervisory interactions with credit unions, the Registry of Credit Unions has found that the introduction of the fitness and probity standards has contributed to an improvement in standards of governance in the sector.

But while many credit unions have embraced these requirements, the Registry of Credit Union remains concerned to see that changes in culture have not fully embedded in all credit unions.

"This is unacceptable given that credit unions are responsible for safeguarding their member’s funds. Where deficiencies in this area are identified, the sector should be in no doubt that the Central Bank will use its full powers, including its enforcement powers under the fitness and probity regime," Ms O'Neill warned.