This week the Paris-based think tank the OECD warned property prices were escalating rapidly and Ireland may be facing another bubble.

Considering the catastrophic damage unleashed by the bust in the financial crisis, the warning should be taken seriously.

But the first issue is that during the downturn Ireland had two simultaneous problems: a credit bubble and a property bubble.

So is it facing the same problem again?

Look at the credit issue first.

This is the perhaps the more dangerous threat.

When the credit bubble burst in 2008, it led to a collapse in the financial system, a €64 billion recapitalisation of the banks by the taxpayer and a bailout of Ireland by the EU and IMF.

It is worth looking at property lending now to assess the risks.

Last month the Central Bank published an analysis of mortgage lending.

It found the average loan-to-value for first-time buyers in 2015 and 2016 was just under 79%.

So, in other words these purchasers were buying with deposits of over 20%.

The other key measure is the size of the loan in comparison to a borrower’s income.

On average, first-time buyers had loans that were almost three times their incomes in 2015 and 2016. That is also far more conservative than lending in the boom.

None of this is very surprising given that the Central Bank introduced rules in February 2015 which limited mortgage lending to insulate against future shocks.

The figures for borrowers who are second and subsequent buyers are even more benign, because they are bringing equity to the property transactions.

So, on the face of it there is no credit bubble in mortgage lending.

Next is the issue of whether there is a property price bubble that is a different creature.

If a property market bursts while there has been prudent lending, in theory, borrowers are less exposed to negative equity.

Also banks should be less exposed to unsustainable mortgages.

But is there a property bubble?

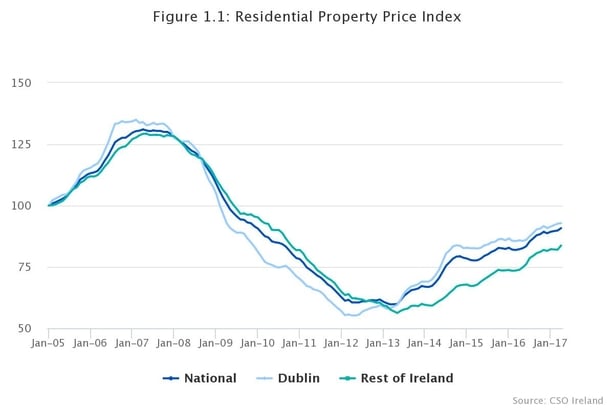

There is no doubt prices are rising quickly.

Nationally the cost of buying a home rose by 10.5% over the past 12 months, according the Central Statistics Office.

However, prices are still down 30.7% from their peak in 2007.

That does not mean there should be any complacency. A property bubble, if indeed one is under way, could be a harmful setback for the economy.

If the Central Bank believes there is a property bubble under way it should act.

But it is also important to remember that the Government has intervened in the market already.

Finance Minister Michael Noonan introduced the Help-to-Buy scheme, which gives buyers a €20,000 tax break that contributes to a first-time buyer’s deposit on a new home.

If there is hard evidence the property market is getting too frothy, revisiting this incentive might be a good start.

Either way the OECD has done Ireland a service by highlighting a significant potential danger, and nobody should ignore the warning.

Comment via Twitter: @davidmurphyRTE