The Fiscal Council is quite clear about what should be done with the proceeds of this month's AIB flotation - pay down debt.

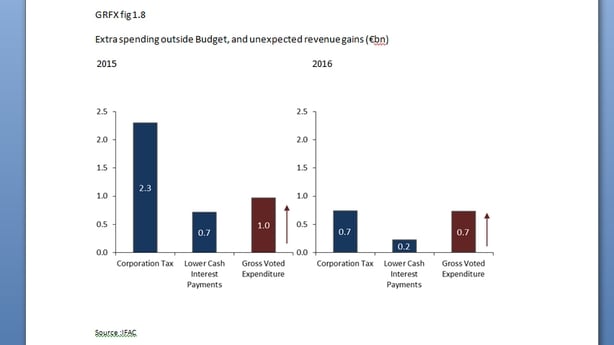

It feels the same way about the stronger than expected Corporation Tax receipts of the past two years. If they had been used to reduce debt instead of increasing (permanently) the spending base, then there would be more room for fiscal stimulus at the end of next year, when the Brexit terms should be clear.

According to IFAC, using the extra Corporation Tax receipts would have reduced debt by €4 billion by the end of 2018 and €8 billion by the end of 2021.

It could also have resulted in the elimination of the budget deficit by now, which would have increased the amount of fiscal space available to the Government now. (On the other hand it would not have relieved the overcrowding crisis in the hospitals in 2015 and 2016, which would have counted against the outgoing government even more than it did in last year's general election. People who can't get hospital treatment have higher priorities than the fiscal balance).

Yes, the Government should be spending more on capital investment, says the new IFAC chair Seamus Coffey, but it must do it in a sustainable way. That is, a way that can be paid for year after year, ad infinitum.

Lobbing €3 billion at a project or ten is fine, until the €3 billion runs out. Then what? Maintenance and renewal of the capital stock is an ongoing cost, and needs to be financed on an ongoing basis. Usually it gets cut first in a downturn, the infrastructure degrades, and then a "catch up" spend is demanded. IFAC says better not to get yourself into a situation where you have to cut capital spending in the first place - run a tight fiscal ship, then you will always have money to spend steadily over the long run.

A second argument they have is that the economy is now growing so strongly that it does not need any stimulus spending from Government. Indeed the Council argues that the Government should be getting ready to "lean against the wind", and prepare to take some money out of the economy in the form of a rainy day fund. The Government Programme already commits it to putting aside €1 billion a year of the fiscal space available from 2019 to 2021 in a rainy day fund. This could then be deployed when needed as a "counter-cyclical instrument".

This would be quite a departure from normal Irish Government practice, which has tended to be pro-cyclical - ie it throws petrol on the flames by spending more money when the economy is booming, then cuts back government spending when the economy is contracting, making the recession worse.

A counter cyclical fiscal policy would work in exactly the opposite way. The Government says it wants to do this. But it means resisting the siren voices of those who say spend more money now. With a housing crisis, a disorganised and high cost health system, an already over-burdened transport system, and the travails of Irish Water, there are no shortage of things to spend money on quickly. But would the public get value for that additional spending, or would it be setting itself up for yet another financial fall?

The Fiscal Council is in no doubt that reducing the government debt is the best use of any additional money from the sale of AIB, or exceptional gains from Corporation Tax. In the latter case, Ireland is heavily reliant on Corporation Tax. It makes up close to 15% of the Government's revenues, compared with less than 8% for the EU average. And las year just ten companies provided 37% of all the Corporation Tax paid in the state.

These two facts render, in IFAC's view, the public finances rather vulnerable. This is all the more so when any unexpected extra CT is snaffled for unbudgeted spending increases, as happened in the past two years.

But the debt is the bigger concern. The big upward revision in GDP as a result of statistical changes in 2015 mean a correspondingly big drop in the debt/GDP ratio - but not of course in the cash amount we owe. Starting this year with a debt/GDP ratio of 78% looks rather good, considering we had been up at 120% just three years ago. And the Euro Area average is 90%. So the debt situation is good, right?

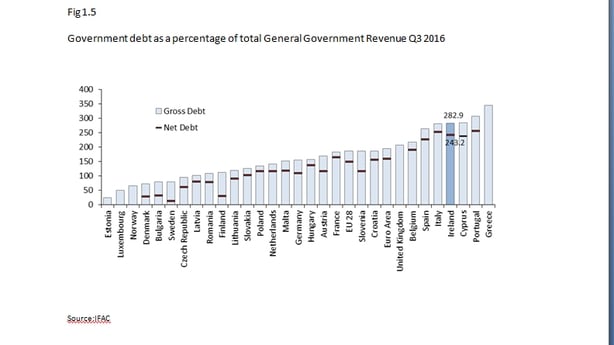

Well not that good, actually. There are other ways to measure debt, and the Fiscal Council likes the ratio of debt to government revenue. Both are policy driven, but the latter is used to pay for the former. The Fiscal Council likes to look at net debt - that is, after cash holdings by the NTMA are subtracted. (The Treasury Agency likes to be pre-funded at least a year ahead, so keeps a fair amount of cash on hand).

By this measure Ireland is a high debt country compared to the rest of the EU. Before the crisis, back in 2006, the net debt to revenue ratio was just under 40% (€26 billion of net debt). At the end of last year it was just over 240%! (€175 billion of net debt). This ratio paints Ireland's debt position as similar to that of Italy (which looks far worse than ours on the debt GDP measure - Italy on 132%, Ireland on 78%).

Only Cyprus, Portugal and Greece make Ireland look good on this basis. On a debt per capita basis - how much in cash terms every man woman and child has as a share of government debt - Ireland is the highest in the EU, and one of the highest in the world. IFAC researchers say on a gross debt basis we are fourth highest in the world, after Japan, the USA and Singapore. On a net debt basis there are no figures for Singapore, so we are in third place, with the USA the most indebted, followed by Japan.

This is not a comfortable position to be in at the best of times. With Brexit and possible changes to the US corporate tax regime coming down the tracks, these are not the best of times from the perspective of a stable revenue stream to service the government debt. The possible revenue shocks from either or both lead the Fiscal Council to urge caution in the planning of the next few budgets, particularly Budget 2018.

The last two budgets breached the fiscal rules. Not enough for the EU to take action against the state. But Ireland is on its hat trick now, and the council points out that it will be harder to argue for exceptional measures to deal with Brexit if the Irish minster comes with a rap sheet of fiscal violations caused by policy choices.

Sticking to the Fiscal Rules will, the council says, provide enough "fiscal space" from 2019 on

(when the budget deficit will be closed, so no consolidation measures will be needed) to both increase spending in line with economic growth, and gradually reduce the debt pile to safer levels. It should also provide enough for a rainy day fund.

The tricky bit will be getting through Budget 2018 and resisting the urge to splash any cash that comes the Government's way. Much will depend on the electoral calculus of the new Taoiseach, and those who give him confidence and supply from the opposition benches.