In the wake of the financial crisis in 2013, Irish households were more likely to spend in excess of their income and leave bills unpaid than other euro zone countries.

An economic letter from Central Bank Senior Economist Julia Le Blanc also shows the household savings rate in Ireland fell to a record low in 2007, ahead of the financial crisis, and increased to more than 14% of income at the height of the crisis in 2009.

Nearly a third (31.3%) of Irish households left some bills unpaid in 2013, compared with a euro zone average of 12.7%.

These households were particularly vulnerable to adverse economic conditions and were at risk of poverty.

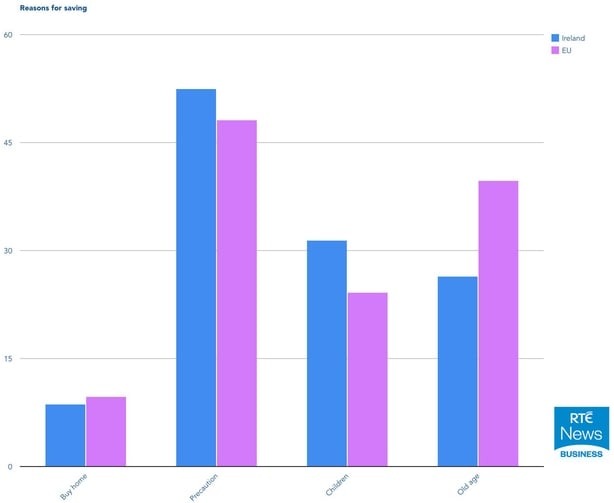

Meanwhile, the study finds that currently 60% of Irish households save at least occasionally as a precaution - the most common motive.

The next most popular reasons for saving are for education and supporting children.

Only 8.7% of Irish households are saving to buy their own home, compared with 9.7% across the euro zone.

Ms Le Blanc's letter provides an overview of savings motives and behaviours of Irish households after the financial crisis.

Meanwhile, the research suggests highly indebted and credit-constrained households save to pay down debts, with some evidence that some households might have difficulty coping with future volatility in income due to levels of household indebtedness.

It highlights financially fragile households, who were spending more than their income or more than what their typical expenses would predict, referred to as 'negative saving'.