With draft budget day for Euro Area states just a few weeks away in mid October, attention is focused on what changes may be in store.

In the case of Ireland, about €300m worth – not much in the context of a €40 billion tax take.

While we look at tax changes from budget to budget, we don’t pay enough attention to tax trends as they develop over time.

Proof of this statement comes in the form of the OECD’s latest publication “Tax Policy Reforms in the OECD 2016”.

This is the first in what is intended to be an annual series, gathering together changes to the tax systems of each of the 34 OECD member states to discern the broad international trends among the most developed nation’s tax systems.

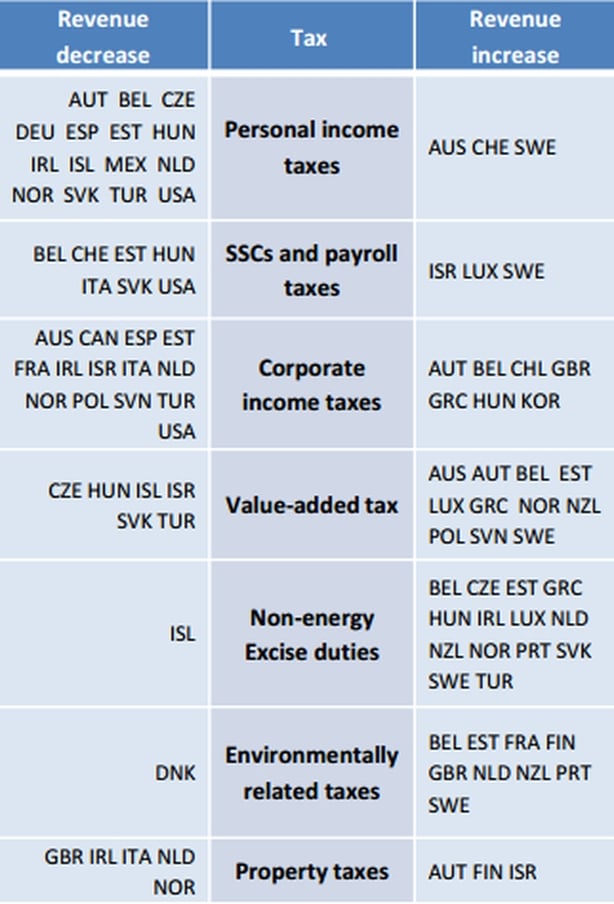

The headline finding is that after several years of hiking taxes to deal with the crisis, governments have now shifted towards using tax policy to boost economic growth.

The good news is that after several years of unremitting increases in personal taxes, 2015 was the year when tax on labour income stabilised, and the majority of reforms legislated to come into effect in 2016 are for tax cuts.

Most of these reforms focused on reducing taxes on low income taxpayers and households with children.

Increasing the standard VAT rate was another clear trend in the aftermath of the crisis, as governments tried to fill in the hole that had opened in their treasuries.

Happily 2015 also marked the end of that trend. Any further increases in VAT take are expected to come from reducing the scope of reduced rates (such as the 9% rate applied to the hospitality and entertainment industry here).

A number of countries did expand their use of reduced rates, thus narrowing their tax base.

The report also notes that 2014 saw the highest average tax to GDP ratio recorded by the OECD since it started keeping score in 1965.

The rate was 34.4%. It has risen during the 90s to peak at 34.2% before declining slightly, then dropping sharply in 2009 to 32.7%.

Ever since, governments in the OECD have been rebuilding their tax take, mainly by increasing personal income taxes and VAT.

But that is the average, and it conceals a wide variance, ranging from below 20% of GDP in the case of Mexico, to above 50% in the case of Denmark, followed by France 45% and Belgium 44.7%.

The USA had a tax take of 26% of GDP in 2014.

Ireland is below average in its tax take as a share of GDP, at 30%. It is the eighth lowest in the OECD, seven places lower than Britain.

The OECD uses pre-Lepronomics numbers for Irish GDP, and yes we do have to take note of the big gap between GDP and GNP.

But even allowing for that it is difficult to make a case that Ireland is a high-tax country by OECD standards – probably just an average one.

The figures also show that while Ireland had an increase in its tax to GDP ratio between 2013 and 2014, there were five other countries that had a bigger increase – three times bigger in the case of Denmark and Iceland, while the Irish increase was not much higher than that experienced by the USA.

Only six countries experienced a revenue decrease during the same period. So our experience was not exceptional.

And between 2010 and 2014, ten countries had a bigger increase in their tax to GDP rations than Ireland.

Countries with high debt to GDP rations tended to have the biggest tax increase during the period.

Prior to the crash, there was a general trend of cutting corporation taxes.

That stopped in the immediate aftermath of the crisis, but according to this publication, the downward trend in business tax is resuming.

Five OECD countries legislated general corporate income tax reductions in 2015, and four more have announced plans for cuts in the coming years.

In the OECD area, corporate income taxes accounted for a relatively small percentage of total taxes – about 9% says the OECD paper, but a paper from the Revenue Commissioners here says the 2014 average was 7.9%.

In Ireland that year Corporation tax accounted for 8.3% of the total tax take (4.2% in Germany, 4.5% in France) while as a share of GDP the Irish take was 2.5% (against 1.5% in Germany and 2% in France).

Several countries have introduced base broadening measures in corporate tax, in particular the report says, to protect domestic tax bases against base erosion and profit shifting.

These changes follow on from the OECD/G20 BEPS process.

(Interestingly, at the recent EU finance ministers meeting in Bratislava, when Ireland was getting a fair old kicking over the Apple tax ruling by DG Competition, it was the OECD boss Angel Gurria who made the strongest intervention in support of Ireland, saying that another Apple could not happen in Ireland because of a series of reform measures that the last government had introduced.)

One area where there has been little reform since 2010 has been property tax (apart from in Ireland, where one was introduced).

The OECD says this suggests the potential to raise revenues in an efficient way, especially through residential property tax, is not being fully exploited.

More property tax, less income tax has been a longstanding piece of advice from Paris (base of the OECD).

The OECD average take from property taxes is 6% of total revenues.

Another area that is under-utilised is Environmental taxes, with few reforms, mostly related to “tinkering with taxes on energy use and cars”.

All of which suggests that states are dutifully implementing tax policy that is broadly in line with the OECD's view that corporation tax and income tax are the most harmful to growth, while property and environmental taxes are the least harmful to growth.

So when you hear people talking about tax reform, you can pretty much guess where reform moves are going to go.

Comment via Twitter: @seanwhelanRTE