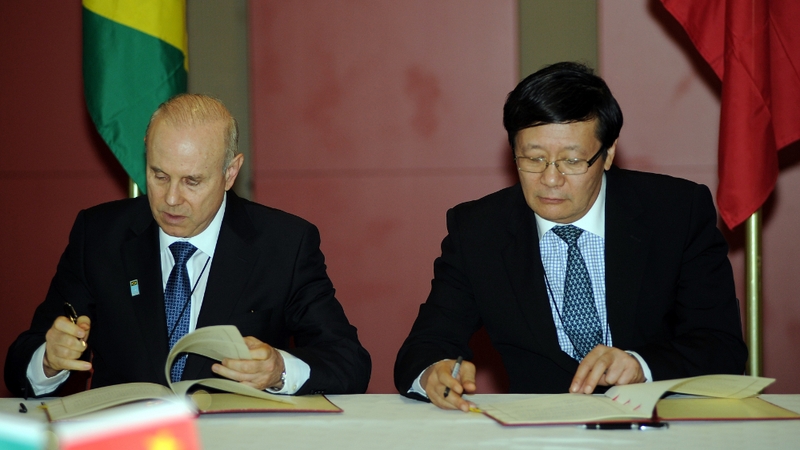

China and Brazil have agreed to trade the equivalent of up to $30 billion per year in their own currencies, moving to take almost half of their exchanges out of the dollar zone.

The three-year swap line agreement, signed before the start of a BRICS nations summit in South Africa, marked a step by the two largest economies in the group to change global trade flows long dominated by the US and Europe.

Brazil, Russia, India, China and South Africa represent together a fifth of global GDP but have struggled to convert their weight into political clout in the international arena.

"Our interest is not to establish new relations with China, but to expand relations to be used in the case of turbulence in financial markets," Brazilian Central Bank Governor Alexandre Tombini told reporters after the signing.

Brazilian Economy Minister Guido Mantega described the deal, called a bilateral currency swap accord, as "a sort of umbrella agreement" but he did not spell out what specific areas or categories of trade would be affected.

Brazil's vast mineral resources and agricultural products have helped fuel China's industrial growth and feed its people while the returns have helped bring a new era of prosperity to the Latin American giant.

Bilateral trade totalled around $75 billion last year.

Of Brazil's $41.2 billion exports to China, iron ore accounted for 34%, while soy and soy products made up 29% and crude oil 12%.

Electronics, machinery and manufactured goods figured heavily in Brazil's $34.2 billion of imports from China.

Brazilian officials have said they hope to have the trade and currency deal operating in the second half of 2013.

Mr Mantega said it would act as a buffer against turbulence in international financial markets dominated by the US dollar.

"If there were shocks to the global financial market, with credit running short, we'd have credit from our biggest international partner, so there would be no interruption of trade," he said.

Chinese officials at the signing made no comments but the People's Bank of China said on its website the currency swap agreement was worth 190 billion yuan ($30.6 billion) and would facilitate trade and investment.

At the Durban summit, the group's fifth since 2009, the heads of state of Brazil, Russia, India, China and South Africa are expected to endorse plans to create a joint foreign exchange reserves pool and an infrastructure bank.

These objectives reflect frustration among emerging market nations at having to rely on the World Bank and International Monetary Fund, which they see as still reflecting the interests of the United States and other rich nations.

The reserves pool of central bank money would be available to emerging economies facing balance of payments difficulties or could be tapped to stabilise economies during periods of global financial crises, according to documents outlining the plan that were obtained by Reuters.

Officials say the BRICS are considering injecting an initial $50 billion into the new infrastructure bank. But the specifics of the scale, location and structure of the institution were still being thrashed out.

"It's a huge job with a lot of difficult issues to be agreed on. In principle, there is some progress," Russian Deputy Finance Minister Sergey Anatolyevich Storchak told Reuters.

The bank would support the ever-growing financing needs in emerging and developing nations for roads, modern ports, and reliable power and rail services.

The BRICS leaders were also due to discuss trade and investment relations with Africa, at a time when many on the economically buoyant continent are seeking more balance and a different focus in trade and investment, especially from the giant of the group, China.

South African President Jacob Zuma welcomed new Chinese President Xi Jinping, who is making his first visit as head of state to Africa.

In Tanzania on Monday, Xi told Africans he wanted a relationship of equals that would help the continent develop, responding to concerns that Beijing is only interested in exploiting its abundant raw materials.